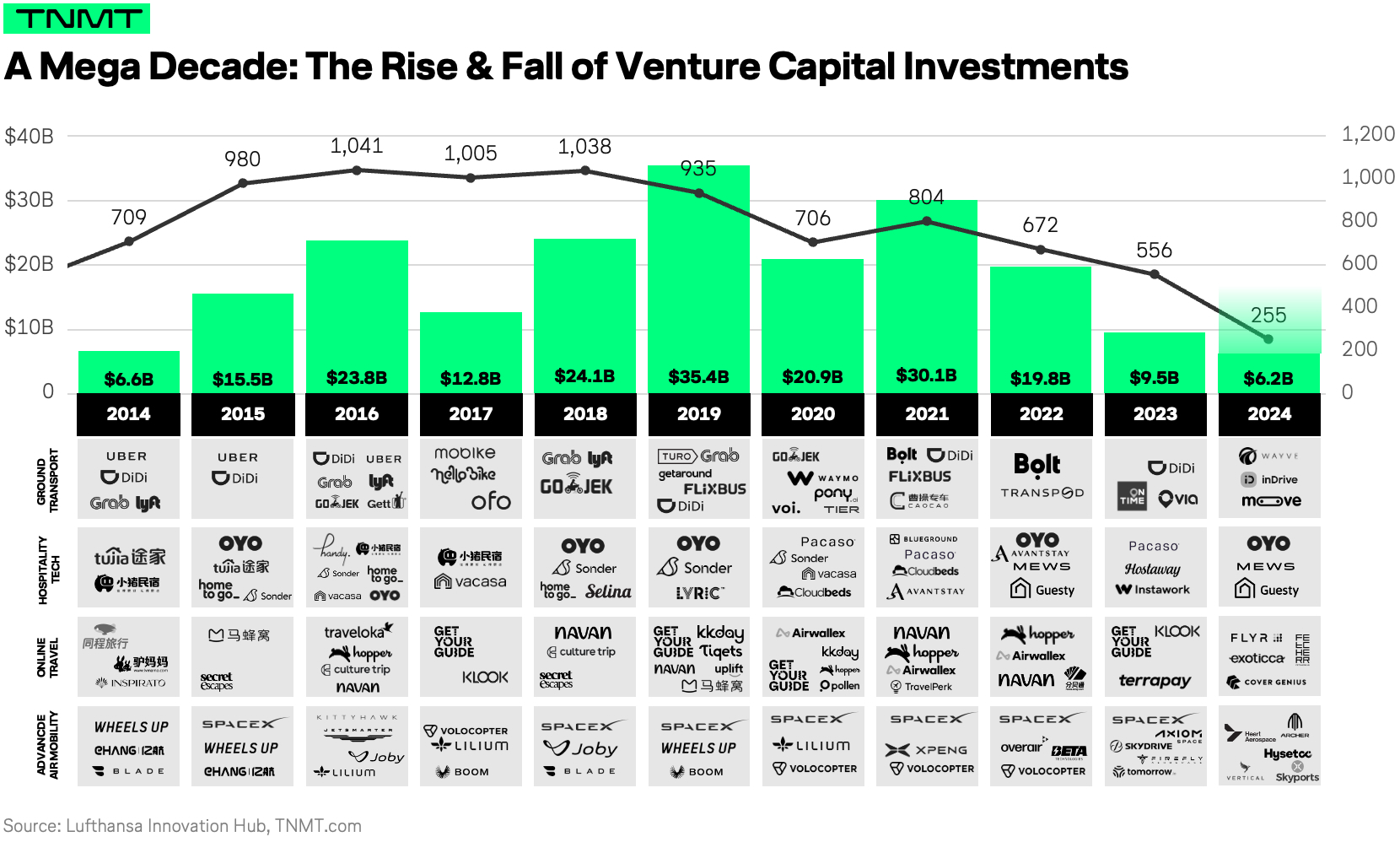

It’s been over eighteen months since we last took a systematic look at venture capital funding in Travel and Mobility Tech.

Our 2024 analysis zoomed in on corporate venture capital, tracking how the industry’s own incumbents (think OTAs, hotels, airlines) were placing their innovation bets through CVC arms, acquisitions, and joint ventures.

This year, we’re shifting the lens back to classical VC funding trends.

- Where are professional startup investors putting their money across the travel and mobility landscape?

- And what does that tell us about the future of our industry?

We’ve long held the conviction that “following the money” is one of the most reliable ways to read where an industry is heading.

Why?

VC funding data reflects where the sharpest investors see market opportunity and where capital actually flows (not where conference panels say innovation is happening).

And that distinction matters.

- Venture capitalists are, at their core, in the business of betting on change.

- They don’t back startups that preserve the status quo.

- They fund the companies they believe will disrupt it.

Every check written is a wager that something fundamental about how an industry operates is about to shift; whether that’s a new technology reaching maturity, a consumer behavior tipping over, or a regulatory landscape cracking open.

The sectors that attract the most VC capital are, by definition, the sectors where investors see the greatest potential for transformation. And transformation is exactly what our TNMT platform is built to track.

So the question of today’s analysis becomes straightforward: How much is travel actually changing?

That’s what we set out to answer in this analysis.

The bearish consensus

If you’ve been following Travel and Mobility Tech analyses outside of TNMT in recent weeks, the answer to that question seems pretty obvious: not much.

Industry discussions on travel funding have painted a consistently bleak picture:

- “We are scraping the bottom of the barrel.” (investor blog)

- “The travel startup funding climate remained challenging throughout 2025.” (Phocuswire)

- “Travel Venture Capital is back, but only for the biggest, safest bets.” (Skift)

All of them point toward a pretty bearish status quo when it comes to change and innovation in travel.

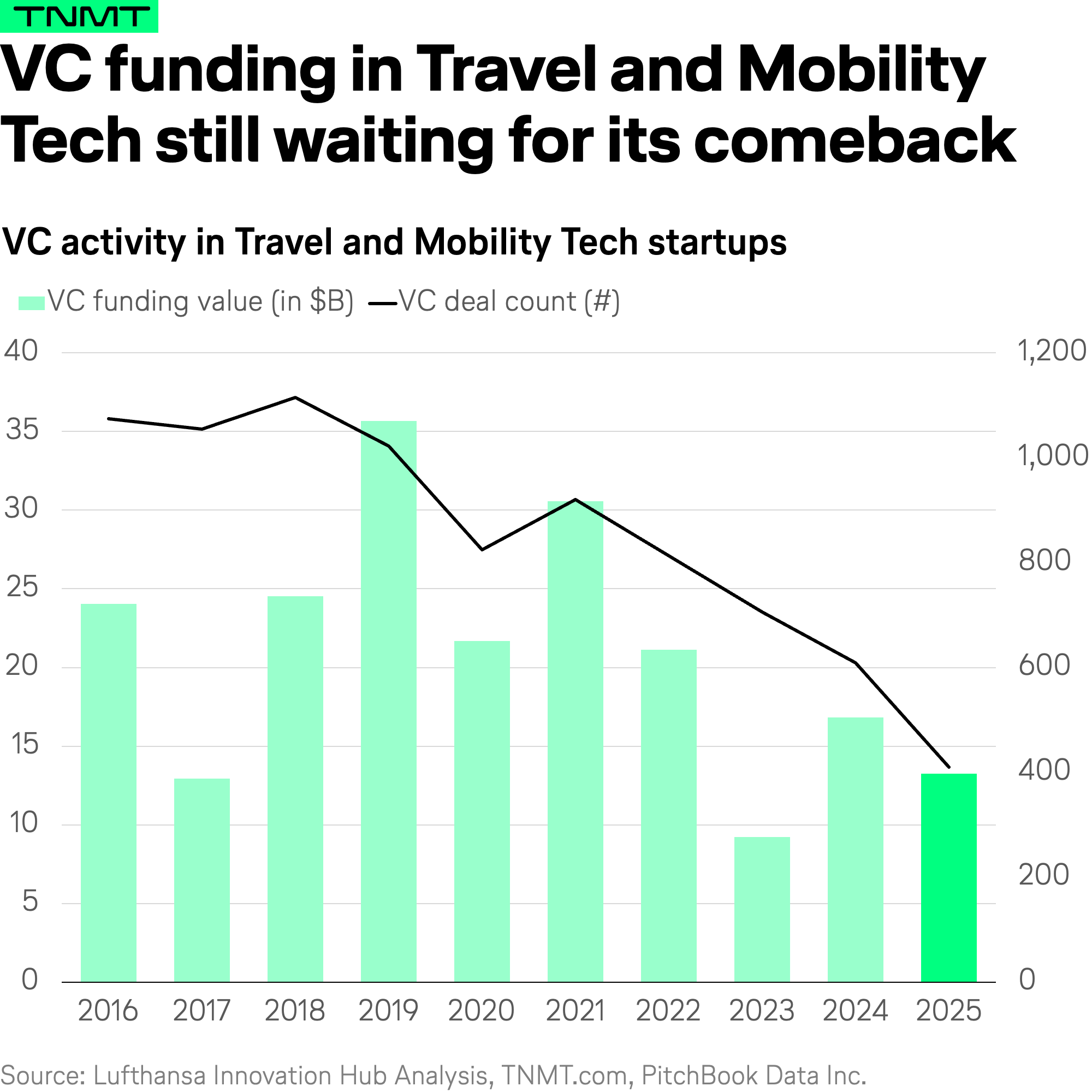

Our own TNMT data support this notion. At least on the surface. Our dataset differs slightly from the sources above, given a more comprehensive and, in our view, more granular definition of the sector. But the top-line picture tells a familiar story.

- Total funding into Travel and Mobility Tech startups in 2025 barely surpassed the lowest annual figures of the past decade (coming in at $13.2 billion USD in 2025).

- And when we measure VC activity by deal count, the picture gets even more sobering: fewer than 400 deals last year, which is the lowest number since our tracking began in 2016, and roughly one-third of the record deal activity we saw in 2018.

Now, critics may rightly argue that this downturn has little to do with Travel and Mobility Tech in particular.

For context: VC funding across industries and sectors has seen a significant slowdown since the pre-pandemic, low-interest boom that peaked around 2021. Since then, the general investment narrative has shifted fundamentally.

- Profitability has replaced hyper-growth as the dominant criterion for investors (a clear departure from the era that gave us VC-subsidized land grabs in e-scooters, food delivery, ride-hailing, and quick commerce).

- Beyond that shift in mindset, several non-sector-specific headwinds continue to weigh on startup funding in general: declining IPO volumes, more sobering M&A exit multiples, geopolitical tensions impacting global value chains, and persistent economic sluggishness across major economies that dampens consumers’ willingness to spend (including on travel).

The travel funding gap is real

So, are the critics right? Is the downturn in Travel and Mobility Tech funding simply a reflection of broader market dynamics? Not quite.

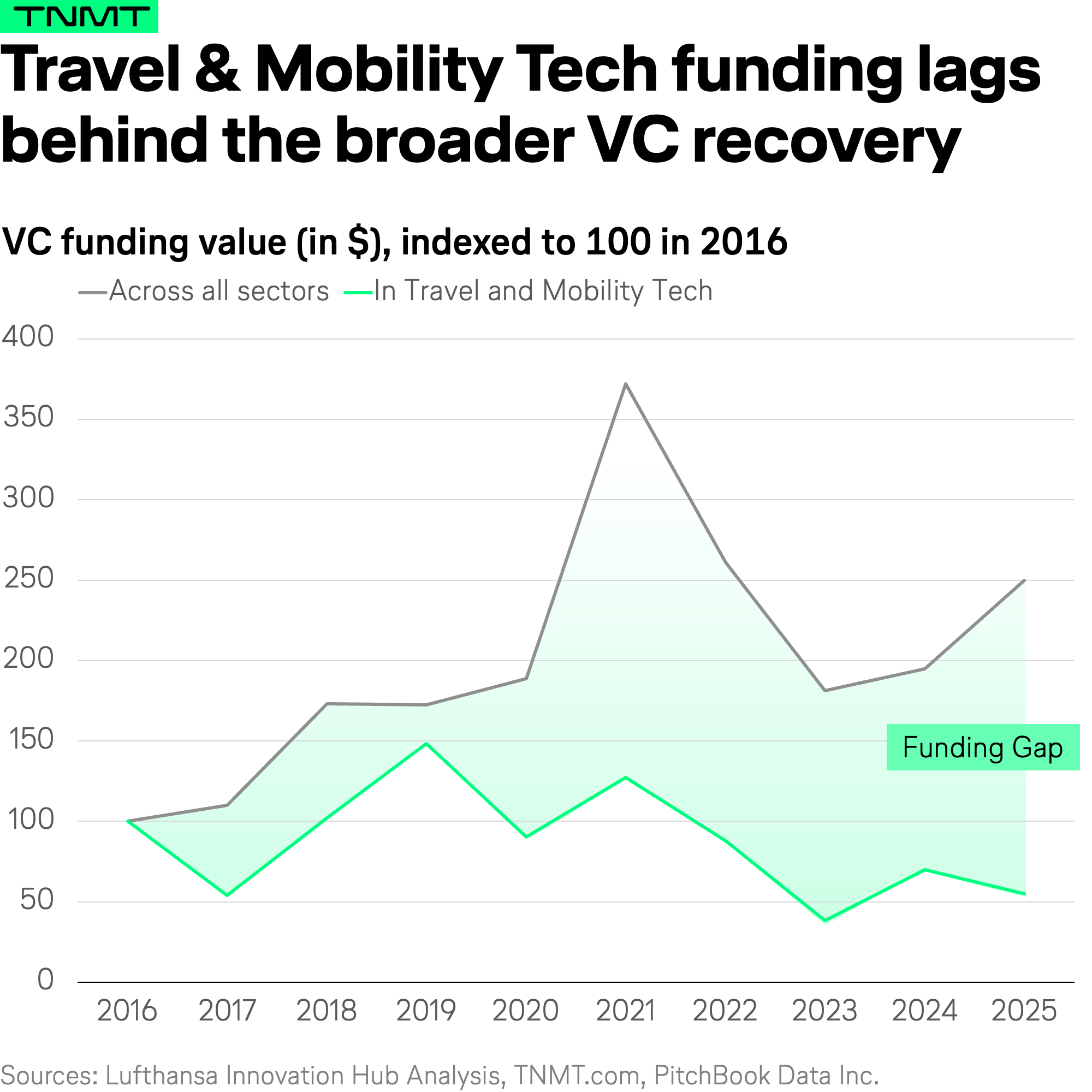

The reality is that funding trends into Travel and Mobility Tech have been disproportionately weak compared to the wider startup ecosystem.

- When we index total VC funding figures from 2016 and compare all-sector funding with Travel and Mobility Tech specifically, a clear funding gap emerges.

- That gap accelerated sharply with the COVID-19 shock in 2020 and has only widened since.

The takeaway: there is less “change” happening in travel than across the broader startup landscape.

This becomes especially apparent when we look at 2025, when global VC figures staged a visible rebound, but Travel and Mobility Tech was unable to follow suit. The implication is hard to ignore. Investors have become disproportionately cautious about betting on travel disruptors; either because they struggle to identify them or because those disruptors simply don’t exist yet.

The safe bet economy

The lack of change also shows up when we look at two additional data perspectives.

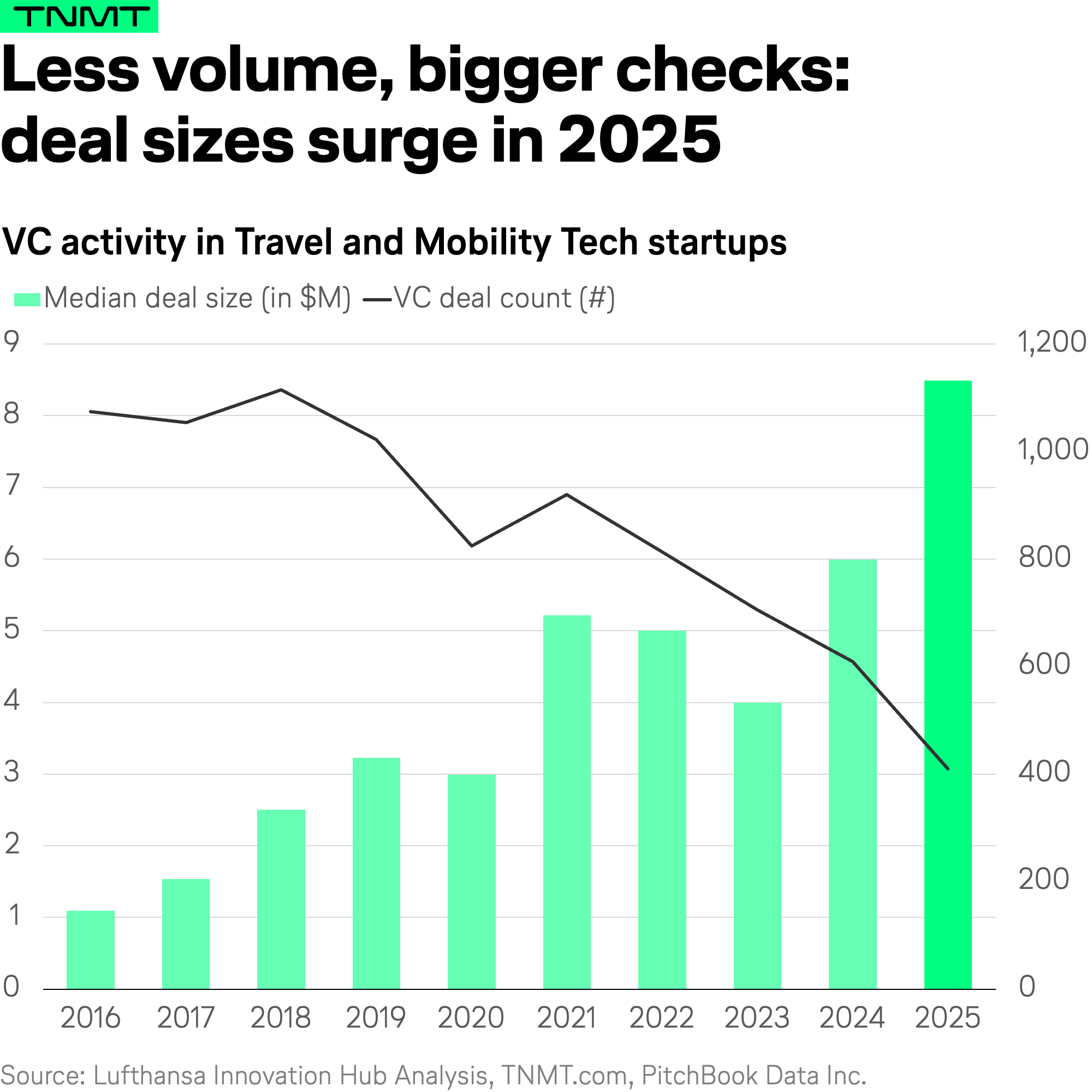

- First, average deal sizes in Travel and Mobility Tech have grown aggressively over the past decade, reaching a new record high in 2025.

- What that means: investors are placing fewer bets on travel startups, but the bets they do place are getting bigger.

This is a clear sign of concentration.

Capital is flowing toward established, well-known startups that investors have already backed in previous rounds (the familiar names, the proven operators, the safe bets).

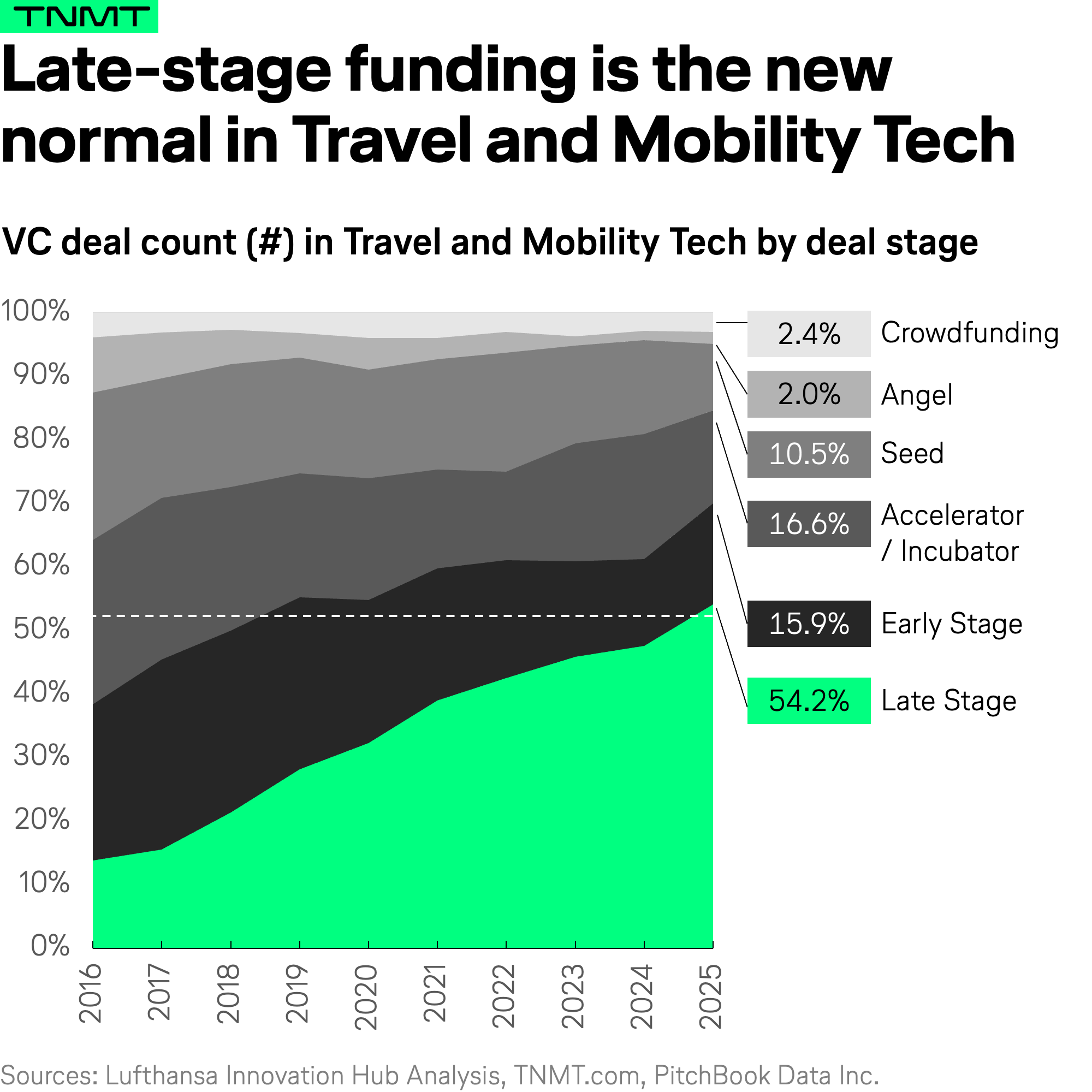

This pattern is confirmed by a second lens: deal activity in Travel and Mobility Tech is heavily skewing toward late-stage funding.

In 2025, more than 50% of all VC deals in the sector were late-stage rounds.

What does that mean?

- The money isn’t going to scrappy newcomers with radical ideas.

- It’s going to scale-ups that have been around for years, building on business models and technologies that were conceived half a decade ago or longer.

Investors aren’t funding the next wave of disruption in travel. They’re doubling down on the last one.

A good example of this trend is Airalo, the Singaporean eSIM provider. Last year, the company made headlines after a massive $220 million USD growth investment, reportedly making it the world’s first eSIM unicorn. An impressive milestone, but hardly a signal of frontier innovation. The technology behind eSIM is anything but new.

- It was first developed in 2012 as a connectivity standard for IoT applications, including smart home and automotive technology.

- On the consumer front, eSIMs became widely accessible in 2017 through smartphones such as Apple’s XS and XR and Google’s Pixel 2 and 3.

Airalo itself raised close to $2 million USD in seed funding back in 2019, targeting its eSIM offering squarely at travelers. And travel has indeed become the primary driver of adoption. According to a GSMA report, 51% of eSIM users in 2025 activated the service while traveling abroad for leisure or personal reasons. So, Airalo’s success story is real, but it’s not a story about disruption. It’s a story about scaling an established technology to serve an already-existing consumer behavior. No new market was created. No incumbent was unseated. The opportunity was identified years ago, and the $220 million USD simply confirms that the harvest phase has arrived, not the planting season.

The AI exception: Where travel is keeping pace

So far, the data paints a discouraging picture. But there’s one area where Travel and Mobility Tech is not falling behind, and it happens to be the most consequential technology trend of our time.

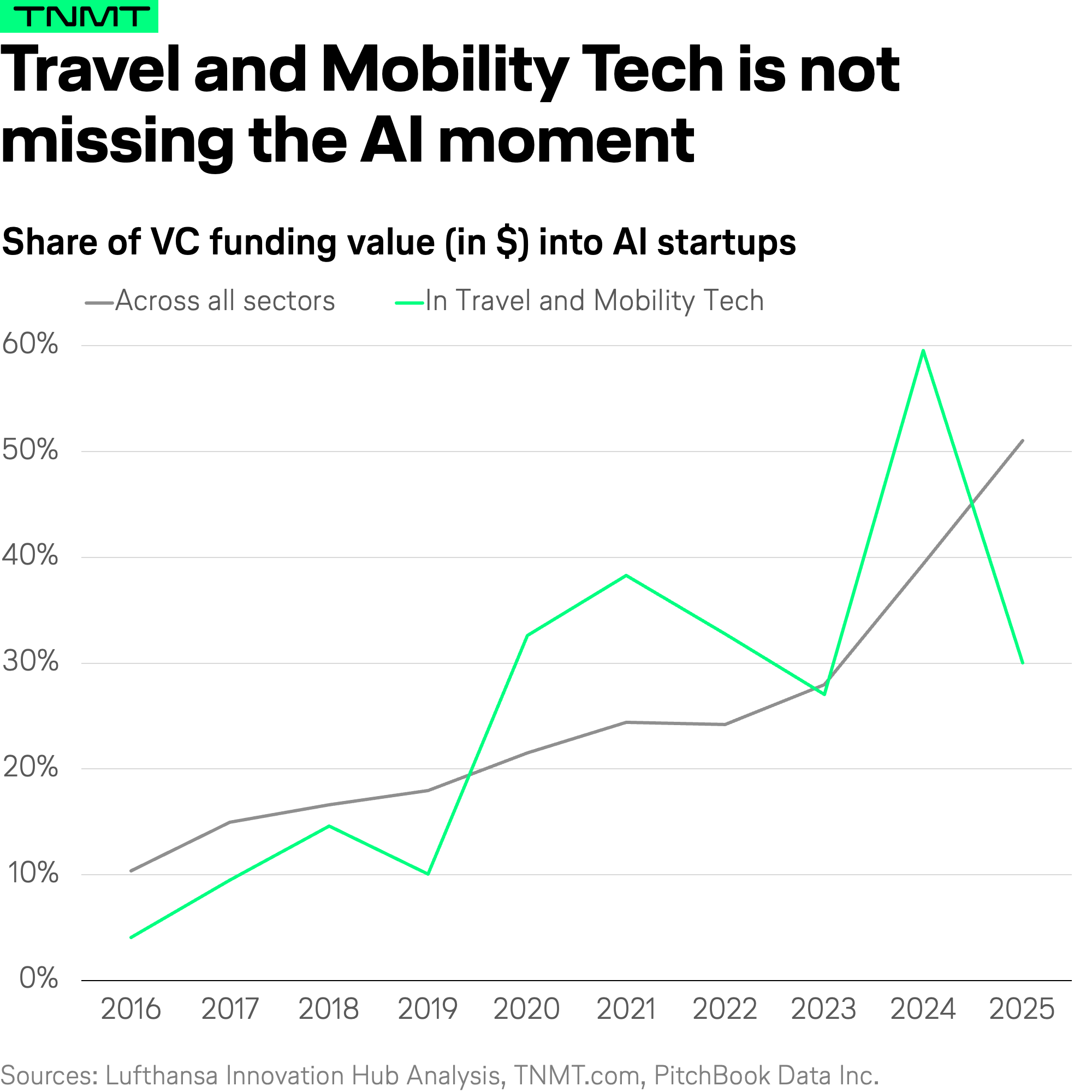

When we compare the share of AI-focused startups raising funding in Travel and Mobility Tech against the broader startup ecosystem, the funding gap we observed earlier disappears.

- In fact, between 2020 and 2024, the share of AI-focused startups within Travel and Mobility Tech raising venture capital was consistently equal to or higher than the share across all sectors.

- In other words: Travel and Mobility Tech has seen as much (if not more) AI funding penetration than the broader startup market.

One caveat: in 2025, Travel and Mobility Tech’s AI share dipped below the all-sector benchmark. But this is almost entirely a distortion effect driven by ultra-mega-rounds into foundational AI providers.

- OpenAI, Scale AI, Anthropic, xAI, and Project Prometheus each raised more than $5 billion USD last year.

- To put that in perspective: these five companies alone accounted for $84 billion USD, roughly 20% of total global venture capital funding in 2025.

Strip out those outliers, and the picture rebalances.

The key message at this point is this: AI has very much arrived in the Travel and Mobility Tech context. Investors recognize AI-powered travel startups as fundable, viable, and relevant. And perhaps more importantly, the opportunity ahead remains massive because enterprise adoption of AI in travel remains in its early stages.

- According to Eurostat, enterprise use of AI technology in transportation had barely breached 10% in 2025 (roughly half the cross-industry average of 20%).

- McKinsey’s State of AI 2025 report tells a similar story: the travel and logistics industry ranks at the lower end of AI agent adoption, with around 4% of respondents reporting that AI agents are scaling or fully scaled across business functions (compared to 5.6% across all industries and 13% in the leading sector, tech).

So AI funding is flowing into travel, but actual adoption on the ground remains low.

That’s a gap, but gaps like this are where the real opportunity lives.

What explains the slow uptake? Several structural factors make Travel and Mobility Tech arguably a harder environment for AI to penetrate than, say, fintech or SaaS.

First, much of the industry is asset-heavy.

- Aviation, along with hotels and ground transport, relies on long-lived, slow-to-change physical procedures, safety protocols, and regulations.

- The need for optimization is enormous, but the path to deploying AI is anything but straightforward.

Second, travel retail is a uniquely complex ecosystem.

- A single booking can involve an airline’s revenue management system, distribution infrastructure, private and business travel agencies, OTAs, and metasearch engines; many of them interconnected through legacy systems like PNRs, GDS platforms, and outdated merchandising standards.

- Changing one link in that chain often means renegotiating the entire chain.

And on the consumer side, trust remains a bottleneck. Travelers may happily use AI to brainstorm itineraries or hunt for deals, but handing over actual booking authority, especially for a €2,000 package tour or a family cruise, is a different story entirely.

Finally, the digital infrastructure gap runs deep across the value chain.

- Tours and activities are still largely booked offline.

- Small and mid-sized hotels often still lack cloud-based systems to manage bookings.

- Ground transport operators struggle with ops digitalization.

And airlines, well. Where data infrastructure is limited, data silos are inevitable. And AI without accessible data is like a car without a road.

The bottom line: AI has massive potential to transform Travel and Mobility Tech. The funding is there. The investor conviction is building. But the industry’s structural complexity means adoption will be gradual, uneven, and hard-won. That’s not a reason for pessimism; it’s the reason the opportunity is still wide open.

And in two sub-sectors, that opportunity is already translating into real funding momentum and, more importantly, commercial traction.

1. Autonomous Driving: From lab to launch

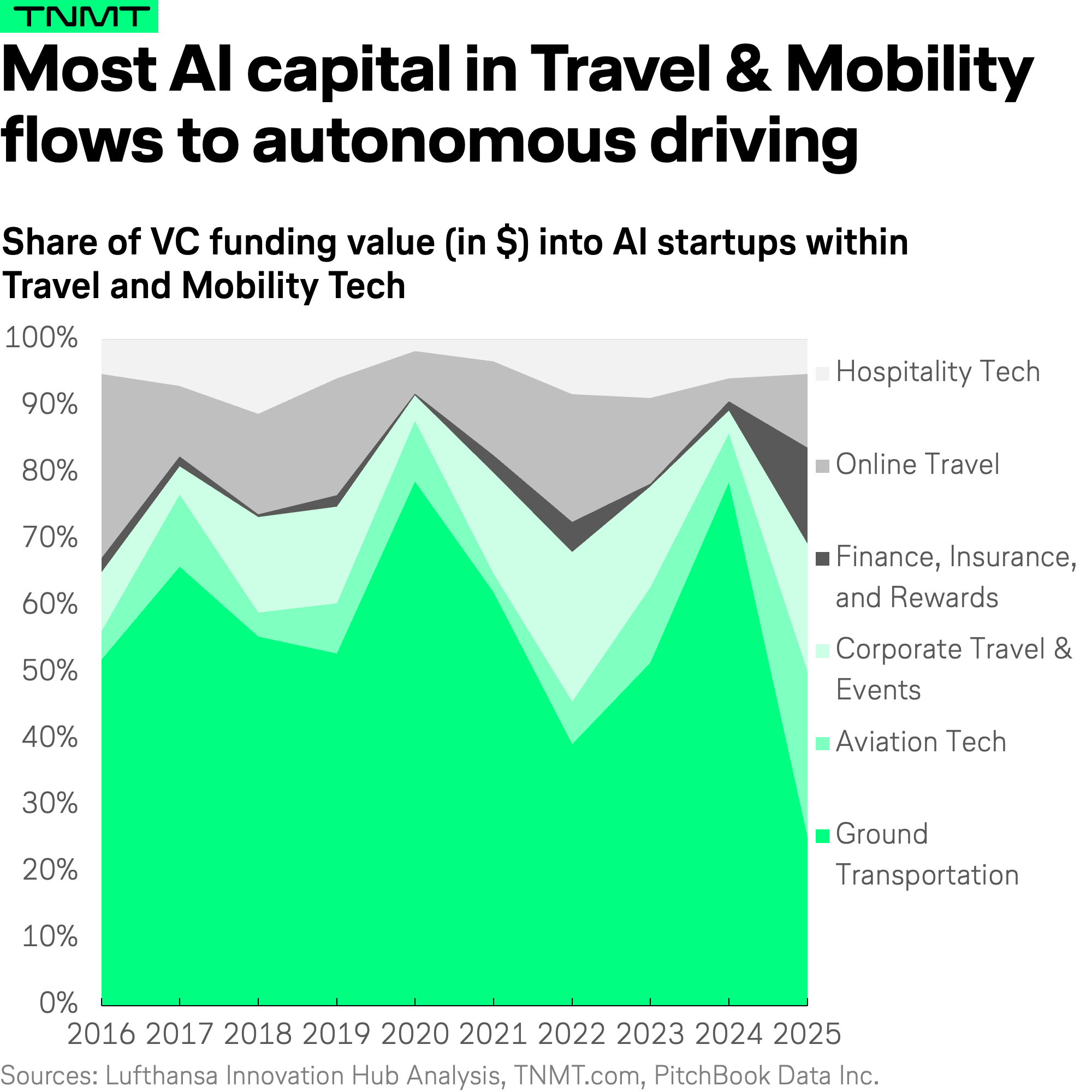

When we break down AI-focused startup funding in Travel and Mobility Tech by sub-sector, one vertical towers above the rest: ground transportation.

Driven primarily by autonomous driving companies and their suppliers, ground transport has consistently captured between 50% and 80% of all AI-related funding dollars in the sector across the years (with significant spikes in individual years).

And those dollars are now translating into real-world disruption. 2025 was the year autonomous mobility shifted from experimentation to commercialization.

- In China, Baidu’s Apollo Go (which began operations as early as 2019) hit a major milestone, reportedly surpassing 250,000 weekly rides in October 2025. The service is concentrated in mega-cities like Wuhan and expanding into suburban districts of Shanghai and Beijing.

- In the US, Waymo launched commercially in 2024 and scaled aggressively throughout 2025, covering five cities and reporting 450,000 weekly rides by year-end. The company has announced plans to expand to more than 20 cities by the end of 2026, including international markets like London.

These real-world proof points have clearly shifted investor sentiment. In the first two months of 2026 alone, the autonomous driving space has already attracted several blockbuster rounds:

- Another $16 billion USD into US-based Waymo.

- $1.5 billion USD into UK-based Wayve.

- $1 billion USD into Canadian Waabi (alongside a newly announced partnership with Uber).

Autonomous mobility isn’t a speculative bet anymore. It’s an emerging market with commercial traction and investor conviction to match.

2. Online Travel’s AI moment: The customer service revolution

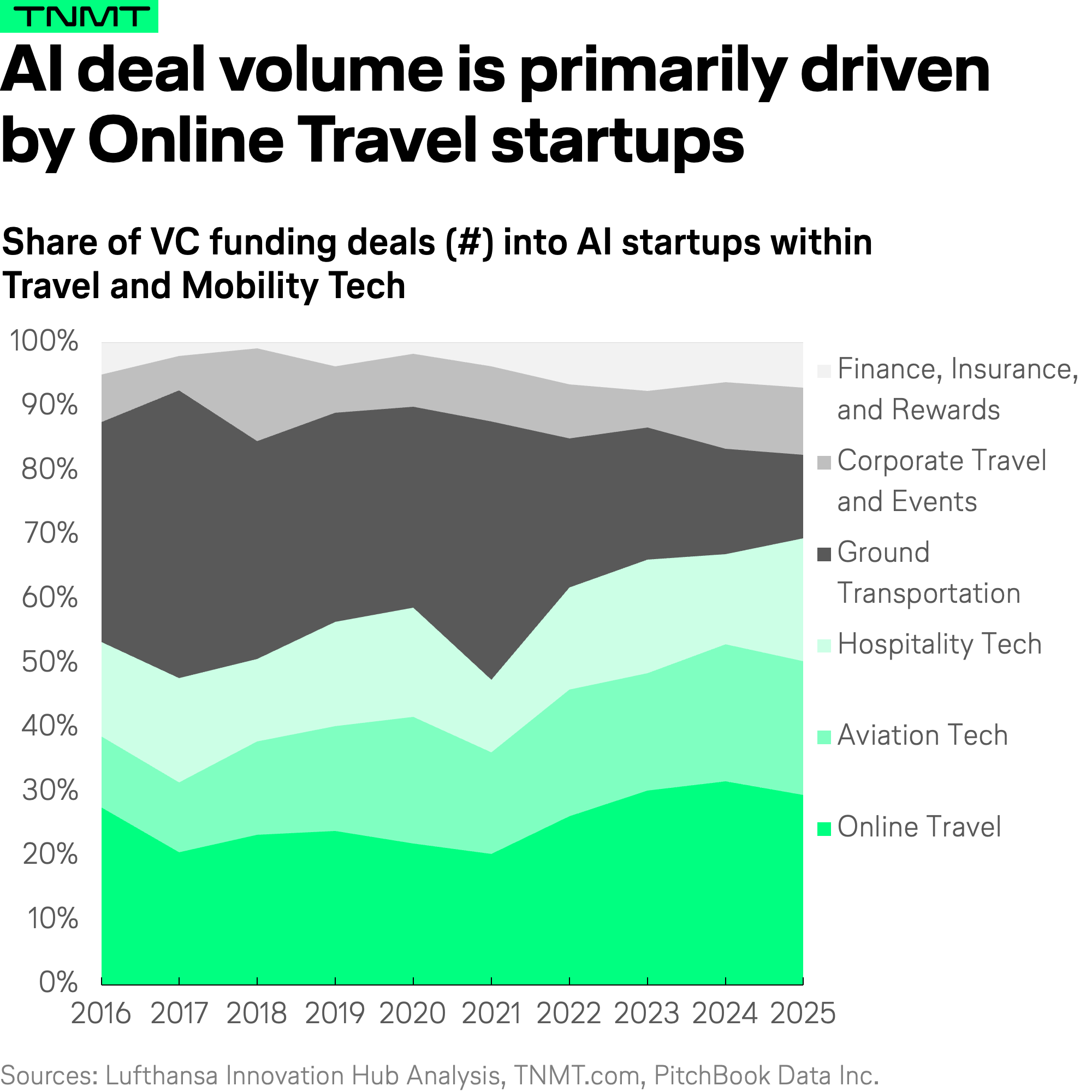

When we look at AI-focused startup funding in Travel and Mobility Tech, not just by deal volume but by deal activity (so the number of individual deals), a different sub-sector rises to the top: online travel.

- In 2025, up to 30% of all AI-related deals in Travel and Mobility Tech went into online travel startups (making it the largest segment by deal count, even ahead of ground transportation).

- That means more online travel-focused AI startups are attracting investor interest than in any other Travel and Mobility Tech sub-sector.

And when you look at what those startups actually do, the reason becomes clear: customer service automation is a dominant investment theme. And for good reason, because online travel players are operating in an environment where growth is getting more expensive by the day.

Take Booking.com. According to Booking Holdings’ Q4 2025 results, the company had a strong year on the top line, with room nights up 8%, gross bookings up 12%, and revenues up 13% compared to 2024.

But the cost side told a different story.

- Total operating expenses increased by 15%, and adjusted fixed operating expenses rose by 10%, driven by adverse FX changes, indirect tax matters, and higher cloud computing costs.

- Marketing expenses as a share of gross bookings also crept up, from 4.2% in Q4 2024 to 4.5%.

- Simply put: making money as an OTA is getting harder, and operational efficiency is becoming a critical lever for profitability.

This is where generative AI enters the picture, and the results are already tangible.

- According to a recent investor call, Booking Holdings reduced customer service costs per reservation by approximately 10% through generative AI.

- CFO Ewout Steenbergen called it remarkable to see a year-over-year decrease in customer service costs while delivering double-digit growth on both gross bookings and revenue.

- This initiative is part of the company’s broader Transformation Program, launched in November 2024, which delivered $250 million USD in savings in FY2025, far exceeding its initial $150 million USD target.

Numbers like that explain why customer service automation is firmly on the industry’s radar.

According to a recent survey of 86 travel executives by Skift and McKinsey, customer experience and service delivery are key focus areas for AI adoption, with nearly 30% reporting they have already implemented agentic AI or plan to within the next six months.

The funding landscape reflects this momentum. In fact, seven of the ten biggest AI startup deals in Online Travel in 2025 were for customer service-oriented companies. That’s not a coincidence. It’s a clear signal of where investors see the most immediate, scalable AI opportunity in travel.

Here’s some context on the top three companies on that list:

- Decagon positions itself as an AI concierge company, helping corporates build voice and chat agents for customer requests. In travel, the agent supports itinerary management, booking support, and loyalty programs. Clients include rental car providers Hertz and Avis, as well as travel rewards company Bilt. Decagon last raised $250 million USD in late-stage funding in January 2026.

- PolyAI, started with a strong footing in hospitality but has since expanded beyond hotels, supporting Hopper’s and Carnival Cruises’ phone-based customer operations. The company maintains a robust hotel vertical, working with properties like Peppermill Resort Spa Casino and Golden Nugget.

- GupShup, founded in 2005, is almost an incumbent in the AI customer support space. With a global presence and close to 20 offices worldwide, the company serves a diverse range of travel clients, including Oyo, Ola, MakeMyTrip, and Cleartrip, offering support across the entire customer journey from acquisition and pre-booking through to post-booking.

Now, if your reaction at this point is “autonomous driving and AI-powered customer service are interesting, but not exactly surprising”, we hear you.

These are the visible opportunities, the ones already attracting headline-grabbing rounds and boardroom attention.

But our analysis also uncovered three less-obvious pockets of innovation in Travel and Mobility Tech.

These are areas where funding signals are still relatively early, incumbents are slow to act, and the potential for disruption is quite significant.

Let’s take a closer look.

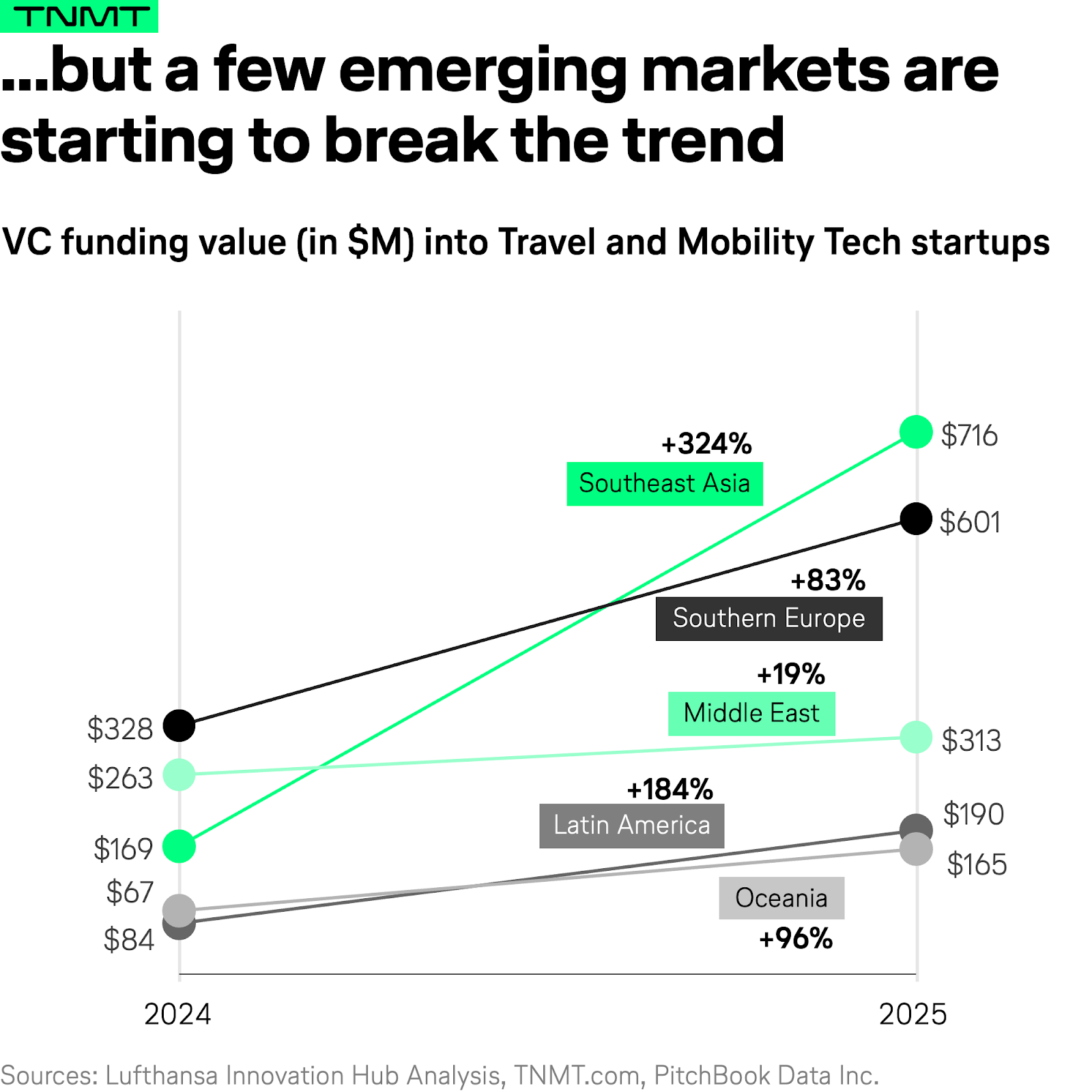

Opportunity #1: The emerging market effect

The first opportunity pocket shows up when we apply a rather classical analysis lens: regional trends.

When we break down Travel and Mobility Tech funding by the three main regions of this world (the Americas, Europe, and Asia), the picture we’ve already described holds true across the board. Deal volumes and deal counts are down across the board. No surprises there.

But when we zoom in further and break those regions down into sub-regions, a more nuanced pattern emerges.

A handful of markets are defying the broader downturn, showing promising growth in VC funding within their respective Travel and Mobility Tech startup ecosystems.

What these five markets have in common: each has seen an impressive tourism recovery since the pandemic, and with it, the rise of an emerging (yet still small) ecosystem of new, travel- and mobility-focused startups that are attracting increasing sums of venture capital.

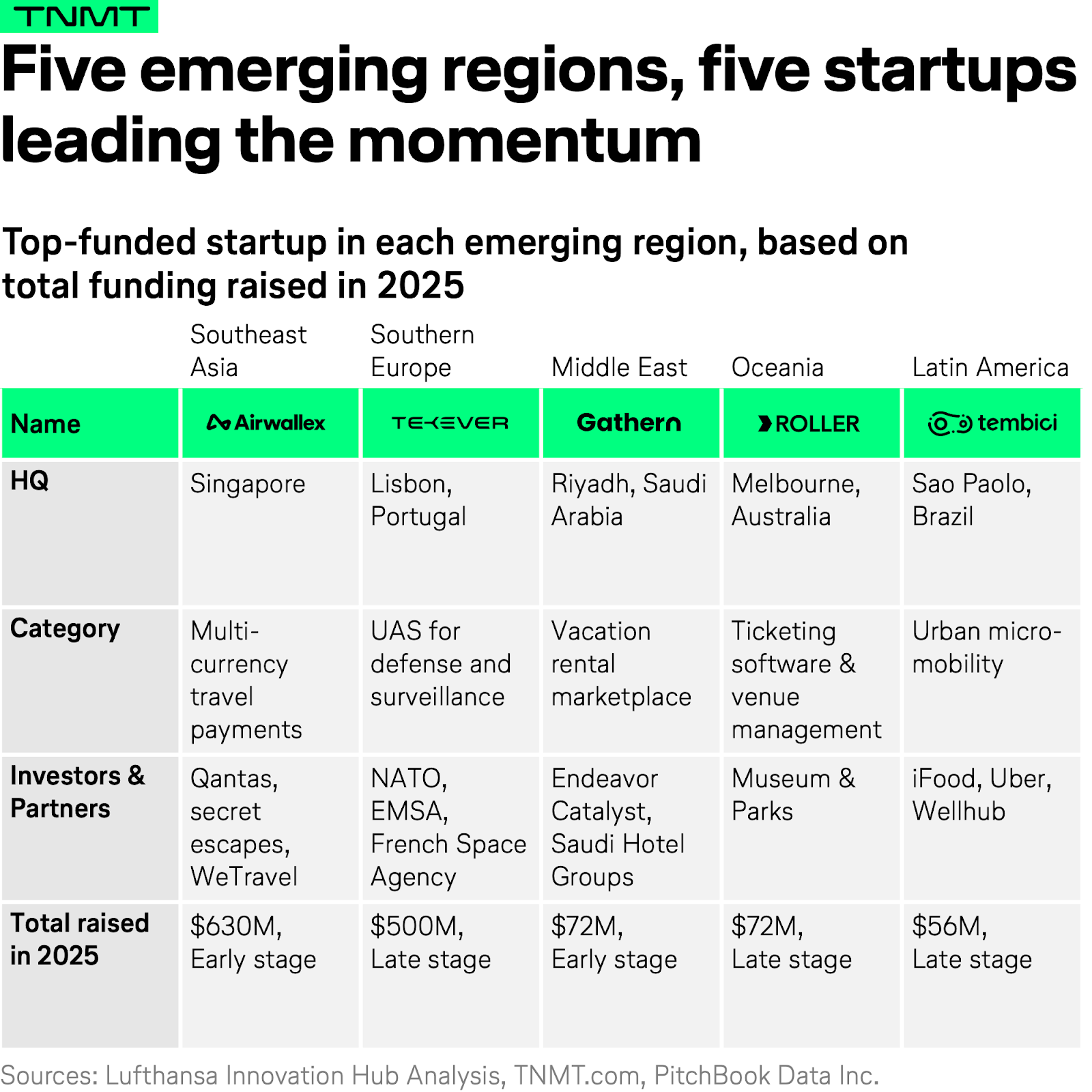

What’s more, each of these five markets has produced its own startup prodigy, meaning one standout company that raised significant funding in 2025, all north of $50 million USD.

And each of these five prodigies operates in a different Travel and Mobility Tech vertical, reflecting the unique characteristics and strengths of its home market.

Let’s look at each of these five markets in a bit more detail.

1. Southeast Asia: The FinTech gateway

Let’s start with the biggest market winner from the above chart. Economies across Southeast Asia have shown strong tourism recovery since the pandemic, though unevenly, due to differing post-COVID reopening timelines, varying visa requirements, and varying degrees of reliance on Chinese tourists (by far the region’s largest source market).

Vietnam and Malaysia, in particular, have posted record tourism years.

Singapore’s tourism economy also stands out, with robust growth in international visitor numbers in 2025.

But Singapore’s significance extends well beyond tourist arrivals.

- Its business-friendly environment, supported by tax incentives, relative regulatory stability, and a mature startup ecosystem, makes it the region’s primary destination for VC funding.

- This is reflected in our data, where the vast majority of Travel and Mobility Tech deals in Southeast Asia land in Singapore, including the region’s standout startup prodigy, which we’ll get to in a moment.

This tourism recovery has translated into significant VC funding inflows. Southeast Asia saw its annual VC funding into Travel and Mobility Tech startups grow from $169 million USD in 2024 to over $700 million USD last year – by far the strongest uptake across all five markets.

Which brings us to the undisputed funding leader in the region: Airwallex. Founded in 2015, the company has raised more than $1.5 billion USD to date at an estimated valuation of over $8 billion USD. That a fintech company (with a strong travel focus) sits at the top is no surprise.

- FinTech has been the dominant funding vertical across APAC for the past decade, despite a massive funding dip during the pandemic and a sluggish recovery since.

- Singapore, centrally positioned as a gateway between Western and Eastern markets, has been a primary beneficiary of this trend, functioning as an intermediary across the region’s diverse languages, cultures, and economies.

- This intermediary role extends naturally to currency: Southeast Asia’s fragmented monetary landscape has shaped Airwallex’s core business model, which centers on global accounts, FX transactions, and corporate cards with multi-currency payment capabilities.

This solves a massive pain point for the travel industry, with its web of partners, agencies, and booking channels spread across the globe.

- According to a recent survey by Skift and Airwallex itself, 75% of travel companies earn more than a quarter of their revenue from cross-border payments, and 88% frequently make payments to suppliers or vendors in foreign currencies.

- Accordingly, Airwallex has built a strong travel vertical and counts an esteemed roster of travel companies among its customers, including Qantas, Uber, Bolt, Bird, Navan, Secret Escapes, WeTrave, and Weski.

2. Southern Europe: Where Defense Tech meets Aviation Innovation

Southern Europe has also seen robust tourism growth. International tourist arrivals were up roughly 3% in 2025 compared to the prior year, with Spain hitting a new record and Greece doing the same.

But the more telling indicator lies in spending. Across the region, tourist spending grew by over 9%, significantly outpacing the growth in arrivals.

This gap is likely driven by a combination of factors:

- More off-season travel.

- Shorter but higher-value trips.

- Greater geographic dispersal across destinations.

- And overall inflation (clearly a factor, but not the only one).

On the VC side, the region is showing equally positive dynamics.

- According to Pitchbook research, Southern Europe’s total annual VC funding across all startup sectors in 2025 was projected to land 26% higher than in 2024.

- Government-backed initiatives are likely fueling this momentum, including programs like Portugal’s Recovery and Resilience Plan, which explicitly targets startup ecosystem development; funding vehicles such as Greece’s EquiFund; and talent attraction schemes such as Portugal’s Tech Visa and Spain’s Startup Law.

This dynamic has carried over into Travel and Mobility Tech, where funding value jumped 83% in 2025 versus 2024, coming in at north of $600 USD million last year.

But what’s primarily driving this travel-related funding momentum?

Not fintech this time.

Something entirely different: Defense Tech.

And the region’s standout startup prodigy tells that story perfectly: Tekever (headquartered in Lisbon, Portugal).

In reaction to Russia’s war on Ukraine and escalating geopolitical conflict globally, European defense expenditure has increased rapidly in recent years (by more than 60% since 2020, to be exact).

- Tekever, a developer of UAS (Unmanned Aerial Systems) for defense and surveillance, is a clear beneficiary of this shift.

- Backed by NATO’s Innovation Fund and the UK’s National Security Strategic Investment Fund alongside commercial investors, Tekever reached unicorn status in 2025 after raising its latest funding round of more than $500 million in May.

Now, a defense-focused drone company might seem like an unusual pick for a Travel and Mobility Tech analysis.

Here’s why we’re tracking it:

Tekever is not strictly a defense company. The company pursues a dual-use approach, meaning its technology serves both civilian and military operations, including maritime surveillance (such as detecting illegal oil spills) and environmental monitoring.

More importantly, defense funding has a proven track record of also advancing aviation innovation. Take Archer Aviation, the US-based eVTOL manufacturer that has raised close to $5 billion USD to develop its electric air taxi for commercial passenger use – a development we’ve covered extensively over the years.

- In 2024, Archer made its first foray into defense by announcing a partnership with Anduril to develop hybrid VTOL military aircraft.

- One year later, it doubled down by acquiring Mission Critical Composites, a manufacturer specializing in advanced composite materials and critical flight hardware for the defense and aerospace industries.

- And Archer is not alone. Companies like Vertical Aerospace and Joby Aviation are also exploring the dual-use potential of their technology through similar partnerships.

The bottom line: in aviation, civilian and military innovation are increasingly intertwined.

We see it as our responsibility to chart these trends when they have the potential to reshape commercial aviation down the road.

3. Middle East: Supply-side ambitions meet geopolitical reality

The Middle East deserves a place on this list as well, but it comes with an obvious caveat.

The region’s current geopolitical situation casts a long shadow over its tourism trajectory.

That said, the numbers leading up to early 2026 have been remarkable.

The Middle East emerged as international tourism’s standout post-pandemic recovery story, surpassing 2019 visitor levels by nearly 40% and reaching a record 100 million international arrivals in 2025.

Much of this growth was fueled by sovereign-backed investment aimed squarely at supply creation.

- Saudi Arabia alone is reportedly investing an unprecedented $800 billion USD into its tourism sector by 2030, including the development of 500,000 hotel rooms and the creation of 1.6 million jobs, with flagship projects like NEOM and the Red Sea Project at the center of this transformation.

- On top of that, the region has benefited from visa liberalization measures, a wave of sports and events tourism tied to mega-events like the Formula 1 Grand Prix, the eSports World Cup, and the Six Kings Slam, as well as the recovery of Chinese outbound tourism.

The VC landscape mirrors this government-led push.

- Sovereign-backed funds like Saudi Arabia’s Public Investment Fund (PIF) and Tourism Development Fund (TDF) are major players supporting startup investments in the region.

- Travel and Mobility Tech funding grew to more than $300 million USD last year, reflecting the region’s growing ambition.

As tourism accounted for a larger share of GDP, supply creation became a dominant theme among local investors. This is especially visible in the region’s hospitality ambitions.

- According to a 2025 report by Lodging Econometrics, the Middle East’s hotel construction pipeline reached unprecedented heights in Q2 2025, with 650 projects totaling 161,574 rooms.

- More than 50% of those projects sit in the upper-scale and luxury segments, with Saudi Arabia accounting for over half of the pipeline.

- This supply-side growth is also evident in the vacation rental space, with cities like Riyadh (+69%) and Dubai (+26%) ranking among the top five globally for vacation rental inventory growth in 2025.

This brings us to Gathern, Saudi Arabia’s leading peer-to-peer vacation rental platform and the region’s current standout startup prodigy in the travel sector.

- Founded in 2016, the company has built a dominant market position.

- The company reportedly turned profitable in 2023 and doubled its revenue in 2024 (a rare combination of growth and financial discipline in the travel startup world).

- To date, Gathern has raised approximately $83 million USD, including a $72 million USD Series B round in August 2025, and is reportedly planning to go public in 2028.

Now, its core advantage is structural, and particularly relevant in the current climate.

While hotel supply is fixed and slow to adjust, vacation rental supply naturally scales with demand, expanding when tourism booms and contracting when it softens. In a region where sovereign-backed hotel mega-projects are locked into multi-year construction timelines regardless of short-term demand shifts, that flexibility could be a genuine competitive moat.

That flexibility will, obviously, now be put to the test.

With geopolitical conflict escalating and travel demand in the region likely to soften in the short- to mid-term, Gathern will need to demonstrate just how adaptable its marketplace model truly is.

4. Latin America: Micro-mobility for mega-cities

Hidden startup market number four takes us to Latin America, where tourism growth has been surging (as well).

- Brazil was the standout performer in 2025, recording a record 9.3 million international visitors (a 37% year-on-year increase), making it the world’s fastest-growing leisure destination by arrival growth rate that year.

- Mexico, the sixth-most-visited country in the world, also marked 2025 as a standout year, with international tourism reaching 98.2 million arrivals (a 13.6% increase over the prior year).

- Expanded air connectivity, a strong events calendar, and growing intra-regional travel are the dominant drivers for the entire region.

On the VC side, after three consecutive years of decline, Latin American venture capital rebounded in 2025, up 14% over 2024. Government initiatives such as Brazil’s Tourism Acceleration Program and Mexico’s equivalent Startup Law framework, alongside a maturing founder ecosystem, are likely contributing to this dynamic.

Looking at Travel and Mobility Tech specifically, funding into homegrown startups grew 184% (so nearly tripling) to $190 million last year.

One of the key beneficiaries? A scale-up called Tembici.

Unlike our other regional champions, Tembici is not a tourism player. It’s a mobility company.

- Headquartered in Brazil, Tembici provides shared access to regular and electric bikes for both private commuters and food delivery workers through a partnership with iFood.

- The company serves urban centers across Brazil, Argentina, Chile, and Colombia, making it Latin America’s leading private operator of docked bike-sharing services and the largest multi-country network of its kind.

- To date, Tembici has raised around $280 million USD in various debt and equity investments.

Structurally, the startup hits a sweet spot. Latin America is simultaneously the world’s most urbanized region and among its most congested.

Over the past 50 years, the region’s urbanization rate has doubled to 80%, with nine out of ten Latin Americans expected to live in big cities by 2050.

Several of those cities rank among the most congested in the world. Accordingly, municipalities across the region are investing heavily in bicycle infrastructure.

- In Brazil alone, São Paulo is constructing over 500 km of bike lanes.

- Rio de Janeiro published a Cycling Expansion Plan in 2022, proposing the addition of more than 1,000 km of cycling infrastructure.

This is Tembici’s core commercial justification: bike-sharing directly addresses urban congestion that public transit alone cannot absorb.

5. Oceania: The Experience Economy’s quiet powerhouse

Hidden startup market number five is Oceania, which has also been going through a steady travel recovery, particularly in 2025.

- Australia welcomed 8.4 million international visitors, up 5.5% year-on-year

- New Zealand crossed 3.5 million arrivals for the first time since the pandemic

But the defining feature of this recovery is not volume. It’s spending. Australia’s total trip spend was up 18% above 2019 levels despite trip numbers still sitting 8% below pre-pandemic benchmarks (reflecting longer stays and a shift toward higher-yield source markets).

On the VC side, Australia’s startup ecosystem raised approximately $3.5 billion USD in 2025 across all sectors, up 24% year-on-year, making it the third-largest VC funding year on record.

This momentum has spilled over into Travel and Mobility Tech, where total funding nearly doubled to $165 million USD in 2025.

The region’s startup prodigy comes from an often overlooked innovation space, actually one that sits at the core of every travel destination: ticketing software and venue management.

Based in South Melbourne, Roller has raised close to $134 million USD across seven funding rounds since its first early-stage fundraise in 2011. Backed by notable global venture and growth firms, including Insight Partners, J.P. Morgan Growth Equity Partners, and RBC Capital Markets, the company operates from offices in Australia, the UK, and the US.

Roller serves a wide array of experience providers and attractions, from adventure parks and amusement parks to museums, water parks, and other leisure venues.

This fits squarely with the travel trends dominating Oceania’s supply side, where nature travel, adventure travel, and passion-driven travel are major themes.

- Booking.com’s 2026 Travel Predictions report named Port Douglas, Queensland (the gateway to the Great Barrier Reef and Daintree Rainforest) as a trending destination.

- Skyscanner’s 2026 Travel Trends report points in a similar direction, with 74% of travelers considering a mountain destination for summer or autumn 2026.

- Hamilton, New Zealand, for example, has reportedly seen an 800+% increase in search interest as it offers a city that blends vibrant urban life with stunning gardens and rich Māori culture, making it a clear winner for cultural immersion and nature travel.

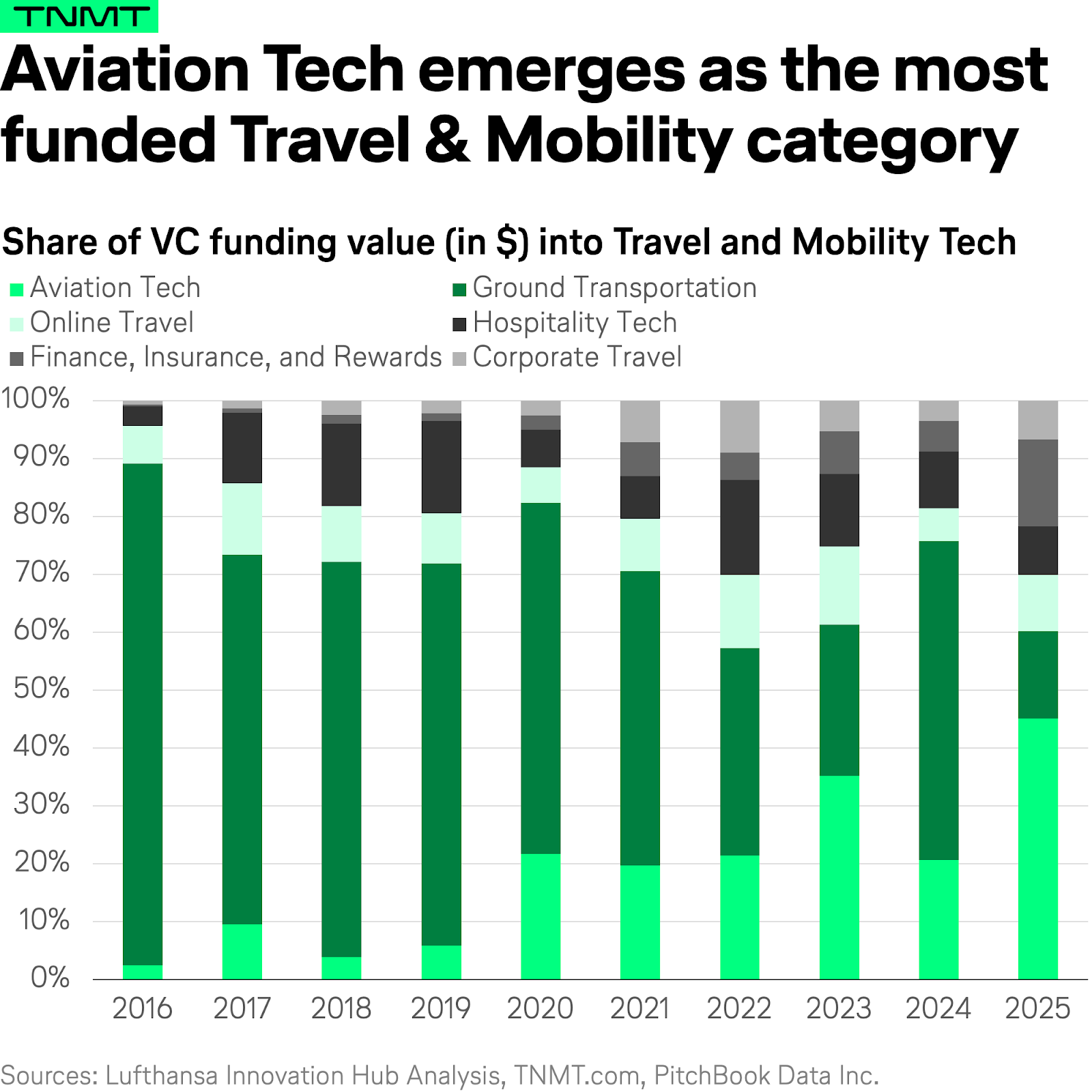

Opportunity #2: Aviation Tech’s new frontier

Beyond regional dynamics, a second opportunity pocket becomes visible when we break down Travel and Mobility Tech funding by segment.

It turns out one sector is gaining outsized relevance within the ecosystem, and it sits right at the core of our industry: Aviation Tech.

Aviation Tech, as we define it, refers to startups driving innovation across the full spectrum of flight (from commercial aircraft and air taxis to airports, digital ground operations, hypersonic and supersonic flight, and space vehicles). If it leaves the ground, it’s on our radar.

- In 2025, close to 50% of all VC funding into Travel and Mobility Tech was captured by Aviation Tech, essentially every second dollar invested.

- And this isn’t just a relative share gain. In absolute terms, Aviation Tech funding grew to $6 billion USD in 2025, a 70% year-on-year increase over 2024.

The interesting question, of course, is what exactly is pushing this momentum. The short answer? Space Travel.

Space Tech had a standout year in 2025. While we primarily track players that work in or support space tourism, the broader industry, comprising parts providers like Honeywell and L3Harris, manufacturers of reusable rockets like Stoke Space, and developers of launch technology like Avio, has shown remarkable and consistent growth.

Why is Space Tech so relevant right now?

One major driver is the usual suspect: defense spending. Reusable rockets, dual-use launch stations, and satellites for intelligence gathering are obvious defense technologies. Accordingly, a major investor in Space Tech is the United States Department of Defense, which aggressively disperses grants alongside the occasional early- and late-stage funding rounds.

In the words of US Defense Secretary Pete Hegseth: “The most important domain of warfare will be the space domain.”

But defense is not the only driver of Aviation Tech. Two more innovation themes stand out:

1 – Reusable rockets and reduced launch costs remain a defining frontier.

SpaceX continues to be the undisputed leader here.

- By late 2025, the company completed its 500th reflight of an orbital booster (the part of the rocket that propels it into space and is typically discarded within the first few minutes of flight).

- For perspective: the only other company to successfully land an orbital-class booster was Blue Origin, which completed its first successful landing in late November of last year.

- No other company worldwide has reached this milestone since, although startups like Stoke Space and Relativity Space, alongside more established players like Rocket Lab, Radian Aerospace, Firefly Aerospace, and China’s Deep Blue Aerospace, are all working toward it.

2 – In addition, AI is accelerating intelligence monitoring from space.

Take World View, a manufacturer of high-altitude balloons for stratospheric sensing and intelligence. These balloons can capture high-resolution imagery for weeks at a time, and World View’s Intelligence Platform processes the enormous volumes of data to provide analytics and decision support.

AI is obviously critical here, and leaning into the generative AI wave, the company announced a partnership with Palantir, known for its cutting-edge AI capabilities.

- Similarly, Planet Labs, a provider of satellite imagery for Earth monitoring, announced a partnership with Anthropic in 2025 to leverage Claude’s reasoning and pattern-recognition capabilities to analyze complex visual information at scale.

- And Google has partnered with Muon Labs, a leading provider of end-to-end space systems, to detect and monitor wildfires.

We conclude with a reminder: history shows that the technologies shaping defense and space today have a track record of reshaping commercial aviation tomorrow. Examples from the past are GPS navigation, composite materials, and fly-by-wire systems. In other words: the innovations that define modern air travel were born outside of it. The Space Tech boom of 2025/2026 may feel distant from airline boardrooms today, but the smart money suggests it won’t stay that way for long.

Opportunity #3: Sustainable Aviation’s quiet comeback

This last one might surprise some readers, especially given how much the climate narrative in the wider travel context has cooled down in recent months.

But fortunately, it turns out that defense spending isn’t the only force propping up Aviation Tech funding.

Sustainability funding continues to be a major investor priority in Travel and Mobility Tech.

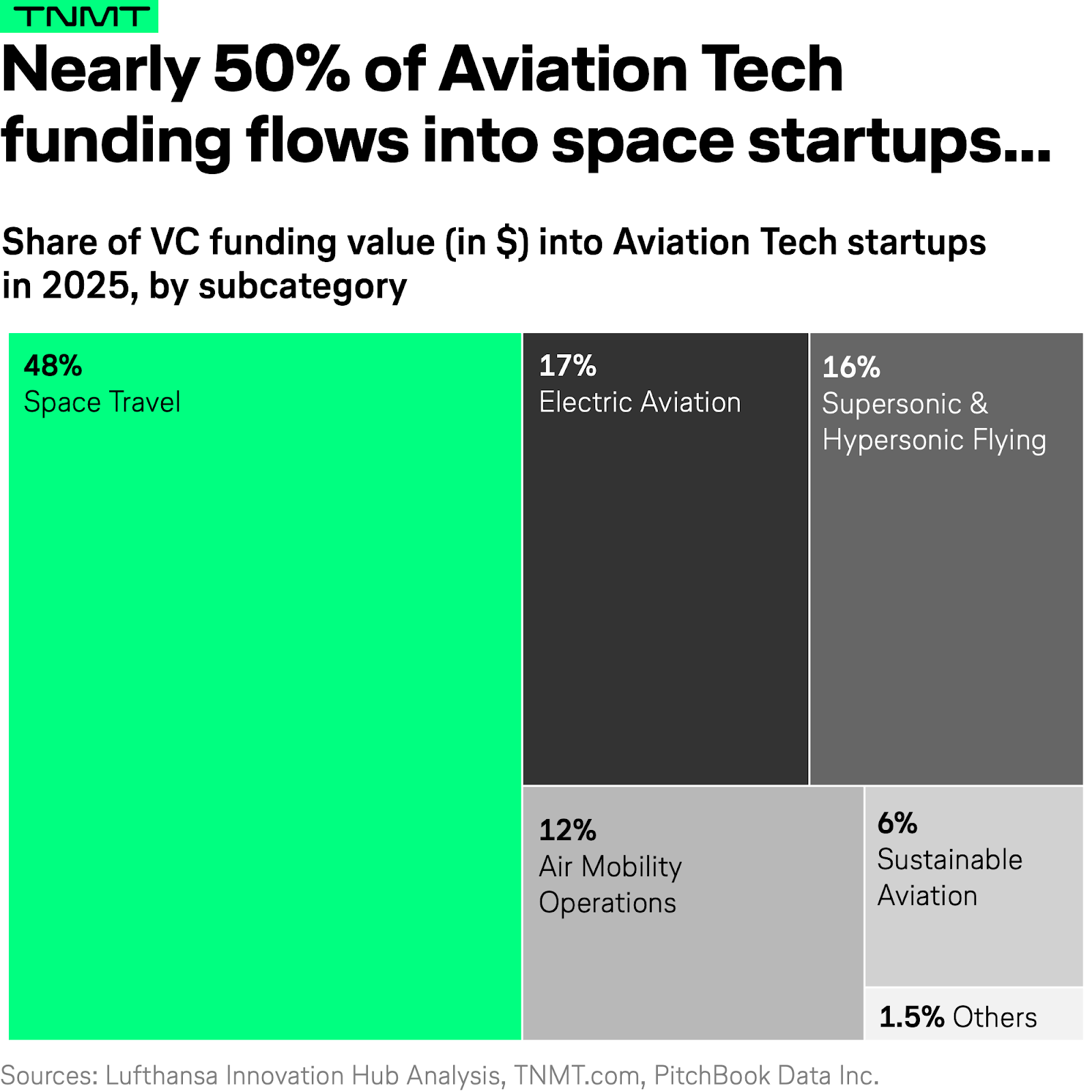

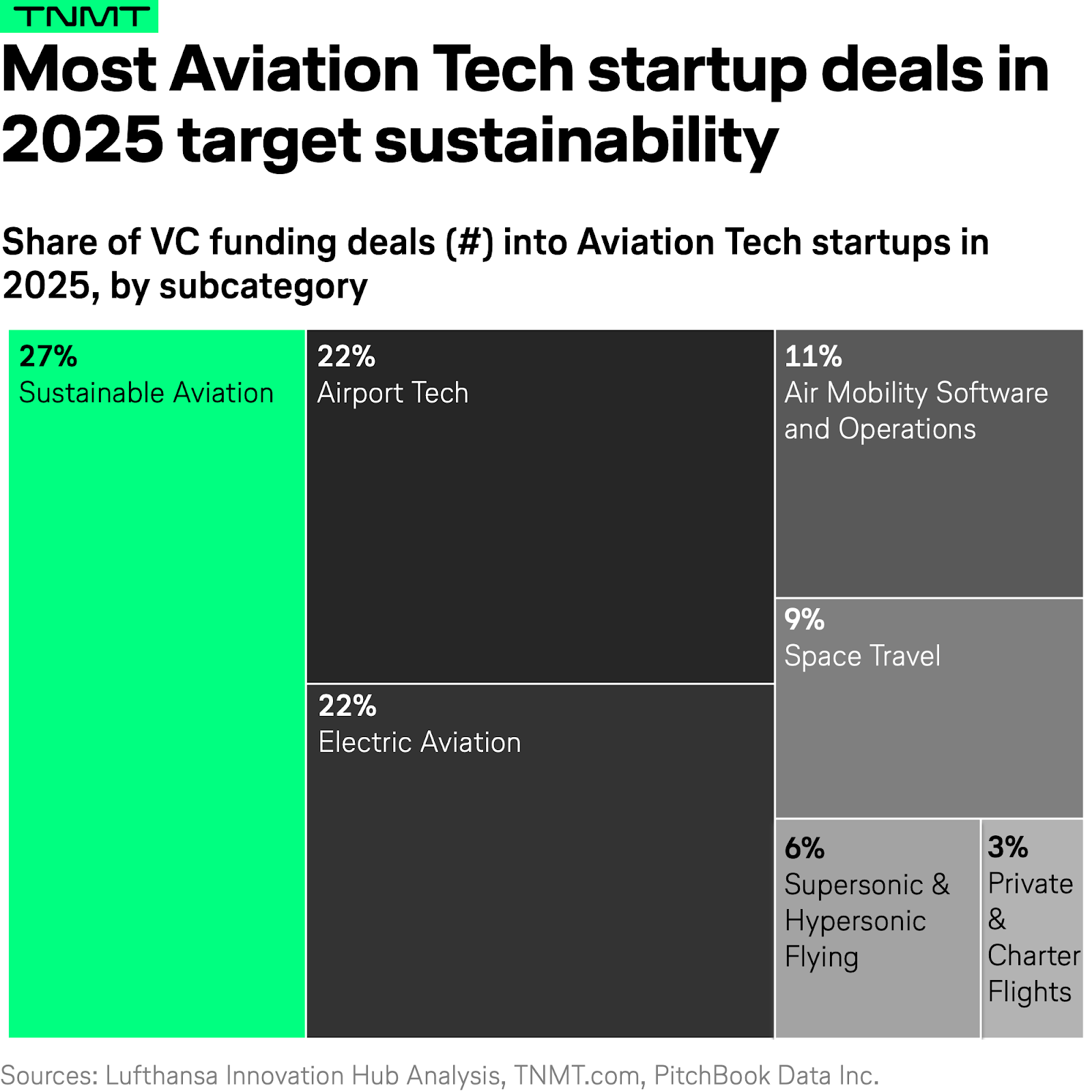

This becomes clear once we break Aviation Tech funding down into its sub-categories by number of deals rather than funding value.

- From this perspective, Space Tech plays a much smaller role (only about 1 in 10 deals go into a Space Tech startup).

- Instead, the largest sub-segment is Sustainable Aviation.

Sustainable Aviation includes all startups and technologies aiming to decarbonize aviation, from hardware innovation to software plays around carbon offsetting and ESG analytics. In 2025, every fourth startup deal in Aviation Tech went into a sustainable aviation company.

Interestingly, the majority of these deals are early-stage, particularly accelerator and incubator rounds that come in at higher volume but lower individual funding values. This is a promising signal. It indicates that a new wave of young contenders is entering the race to help decarbonize aviation, which remains one of the industry’s most pressing and complex challenges.

Side note: the second most active category within Aviation Tech by deal count in 2025 is Electric Aviation, which overlaps with Sustainable Aviation to some extent, reinforcing the broader momentum around cleaner flight.

Interested to see who these new sustainable Aviation Tech startups are?

Here’s a ranking of the ten most relevant companies by total funding raised in 2025.

Looking at the leaders of this table:

JetZero, founded in 2020 and headquartered in Long Beach, California, is developing advanced aircraft designed to improve efficiency and operational versatility through its commercial blended-wing-body concept.

- The company claims up to 50% better fuel efficiency and lower carbon emissions than conventional aircraft.

- JetZero has raised more than $220 million USD to date and counts notable investors such as Alaska Star Ventures, United Airlines Ventures, 3M Ventures, and Northrop Grumman among its backers.

Aether Fuels, founded in 2022 and based in Singapore, develops sustainable liquid-fuel technology to decarbonize aviation and ocean shipping.

- After raising close to $37 million USD in June 2025, the company completed another early-stage round in early 2026, totaling $15 million USD with participation from IAGi Ventures.

- The new funding will reportedly support plans to launch the first commercial sustainable aviation fuel facility in Singapore.

BeZero Carbon, founded in 2020 and based in London, operates a global rating agency focused on the voluntary carbon market.

- The company provides independent, risk-based, project-level carbon ratings for investments in carbon projects, including aviation’s CORSIA scheme.

- BeZero has raised more than $100 million USD to date and counts Japan Airlines Company among its investors.

The bottom line

So, what to make of all of this?

Venture capitalists bet on change. And on the surface, the data suggests they don’t see enough of it in travel. That’s not entirely unfair.

Travel and Mobility Tech is one of the most structurally complex industries in the world, layered with legacy distribution systems, fragmented stakeholder networks, heavy regulation, and physical assets that don’t transform overnight.

Change here is harder, slower, and messier than in pure software sectors. The aggregate funding numbers reflect that reality. But aggregate numbers hide as much as they reveal.

When we look beneath the surface (at specific regions, sectors, and technologies), a different picture emerges.

- Autonomous driving is commercializing.

- AI is delivering measurable ROI in customer operations.

- Emerging markets are producing homegrown champions.

- And a new generation of founders is taking on aviation’s decarbonization challenge at the earliest stages.

The change is there.

It’s just not evenly distributed, and it never is in an industry this complex.