The airline industry has spent the past few years moving from one pressure point to the next.

- Passenger demand came back after COVID, but not evenly across regions, routes, and customer segments.

- At the same time, cost pressure intensified, with airlines exposed to volatile fuel prices, rising labor costs, maintenance constraints, airport charges, and broader inflation across the aviation value chain.

- Operations were stretched during record-busy summer seasons, while labor shortages, air traffic control constraints, and aircraft delivery delays made it harder to add capacity smoothly.

- Sustainability also moved from a long-term ambition to a boardroom issue, as SAF, emissions targets, regulation, corporate customer expectations, and passenger scrutiny became a more visible part of the airline narrative.

- More recently, geopolitical instability has forced airlines to adjust networks, avoid restricted airspace, rethink capacity deployment, and manage fuel and currency volatility in a market that feels increasingly unpredictable.

For airline executives, strategy has become less about choosing one big priority and more about deciding what deserves attention when almost everything feels urgent.

To understand where long-term priorities in the airline industry are really shifting, we need to separate the signal from all of that noise.

Carefully managed interviews, investor presentations, and press releases announcing new products and services all have value. But they are controlled formats. They show the narrative airlines want to project. What they do not reveal is which priorities hold up under commercial pressure, especially when executives have to connect strategy to demand, yields, unit costs, capacity plans, capex, margins, and strategic guidance.

That is where earnings calls become especially useful.

Earnings calls force strategy into a commercial context.

- Executives are not only explaining what they care about.

- They are explaining how those priorities translate into business performance and, most importantly, future earnings.

- At the same time, analysts and investors test that logic in real time by asking where growth will come from, how margins will be protected, and which risks could derail the plan.

This makes earnings calls one of the most underused sources of strategic intelligence in the corporate context.

That said, a single earnings call can still be noisy, though.

But viewed over several years across many airlines, these conversations become a valuable record of shifting management attention.

By analyzing how airline earnings calls have evolved, we can trace where the industry’s long-term priorities are moving.

And that’s what we did.

How we measured airline management attention

For this analysis, we analyzed 17 quarters of earnings-call transcripts, from Q1 2022 to Q1 2026, covering ten of the largest publicly listed airline groups by last reported revenue that hold English-language earnings calls, namely:

- Delta

- United

- American

- Southwest

- Lufthansa Group

- IAG

- Air France-KLM

- Ryanair

- Turkish Airlines

- And LATAM Airlines.

We then developed a curated set of 12 topic clusters that cover the major strategic themes discussed across all these airline earnings calls. Each cluster was defined by a specific list of keywords and phrases, with clusters kept mutually exclusive as far as possible.

- Every keyword or phrase occurrence was counted using whole-word, case-insensitive matching.

- To keep the analysis focused, we relied on specific phrases where possible, such as “capacity discipline” rather than broad, generic terms like “capacity.”

- Each topic cluster was then expressed as a share of all tracked mentions, allowing us to compare how airline management attention has shifted over time.

This approach does not capture every nuance of executive strategy communication.

But it gives us a structured proxy for what airline leaders and investors repeatedly bring into the earnings conversation, and how that agenda has changed over the years.

Commercial fundamentals still dominate the airline agenda

Enough upfront context. Let’s look at the data, starting with the simple topic overview.

And, admittedly, the first finding is not exactly shocking.

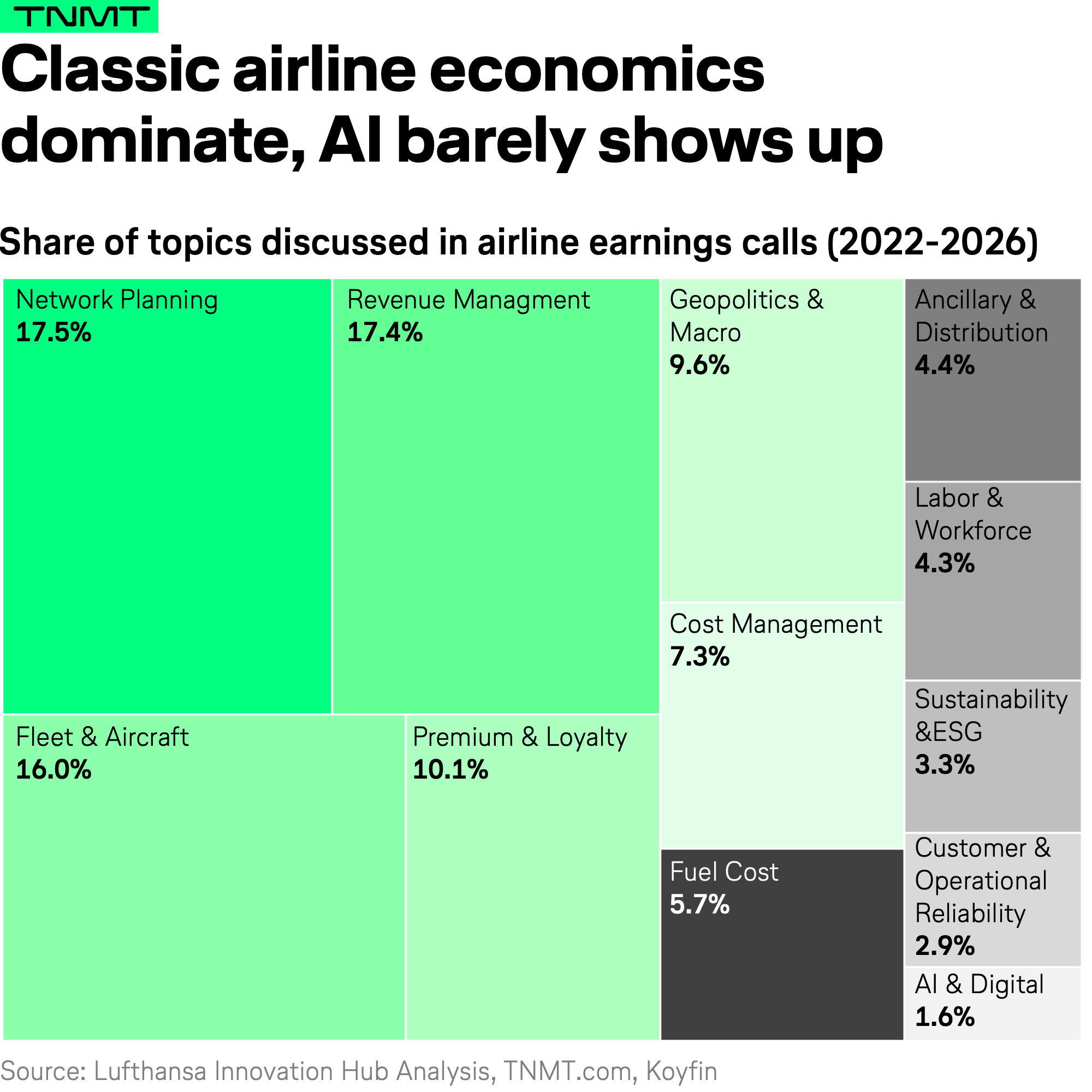

Across all analyzed earnings calls, classic airline management topics dominate the conversation.

- Network Planning accounts for the largest share of tracked mentions, at 17.5%. This includes discussions around route decisions, capacity deployment, market openings, hub strategy, and the constant balancing act between supply and demand (all of which directly shape load factors, yields, aircraft utilization, and ultimately profitability).

- Close behind is Revenue Management, essentially the airline art of pricing, so yield optimization, and capacity discipline.

- Fleet & Aircraft topics follow at 16.0%, covering themes such as aircraft deliveries and retirements, and the capex decisions behind future growth.

- Premium & Loyalty discussions add another 10%, reflecting the growing importance of high-value customers, premium cabins, and loyalty economics for airline profitability.

Together, these four topics account for roughly six in ten tracked keyword mentions.

That makes sense. Earnings calls are, by nature, about commercial and financial performance.

And few themes connect more directly to airline economics than where airlines fly, how they price, which aircraft they operate, and how effectively they monetize their most valuable customers.

But the more interesting perspective begins when we move beyond the overall ranking and look at how these themes have changed over time.

Momentum tells a different story

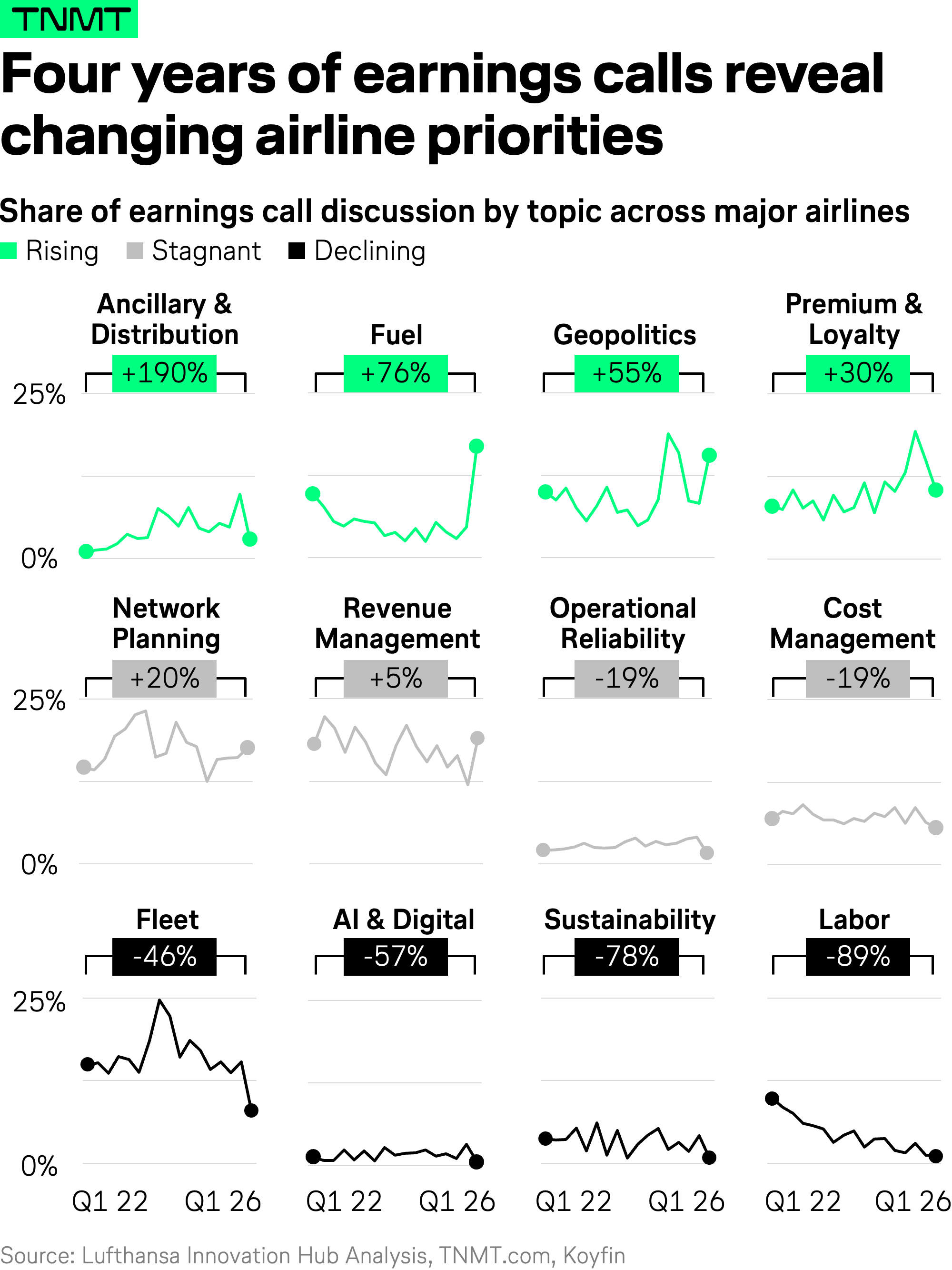

When we map earnings-call topic coverage quarter by quarter, from Q1 2022 to Q1 2026, the picture becomes much more nuanced.

- Some themes clearly gained attention.

- Others remained broadly stable.

- And a few lost significant momentum.

This is where our analysis becomes more insightful because among the four classic airline management topics that dominate overall earnings-call discussion, only one made it into the group of clear growth themes.

That standout is Premium & Loyalty, which increased by 30% across the analyzed period.

The other major growth themes are less traditional, but highly revealing:

- Ancillary & Distribution surged by 190% over the past four years

- Fuel rose by 76%

- And Geopolitics increased by 55%.

What that shows:

- The airline earnings conversation is not necessarily becoming “more commercial” in the classic sense.

- Instead, it’s becoming more focused on the pressure points that sit around the core airline business, for example, how airlines monetize beyond the ticket, how they manage external cost shocks, and how they react to geopolitical disruption.

That is where the real shift in management attention begins to show.

So let’s look at the four growth areas in more detail and unpack the concrete drivers behind them.

Because in each case, the rise is not driven by one single storyline. It reflects several underlying shifts (some sequential, some overlapping) that together pushed these topics higher on the airline earnings agenda.

1. Ancillary & Distribution moves into the strategic spotlight

The clearest growth story is Ancillary & Distribution. It is by far the fastest-growing topic in our analysis, with tracked mentions up 190% since early 2022. Without Q1 2026, when fuel and geopolitics temporarily took over the conversation, Ancillary & Distribution would have been close to a tenfold growth story.

The primary driver is the ongoing unbundling of the airline product.

Early in the period, the topic barely showed up. Unbundling was still largely viewed as a low-cost carrier specialty, while many legacy airlines treated bag fees, seat selection, and other paid add-ons as secondary revenue levers rather than core strategy.

That changed over the following years.

- Extra-legroom seats, bag fees, paid seat selection, and upselling mechanics became more prominent as airlines sought new ways to monetize the same passenger beyond the base fare.

- Southwest is perhaps the most symbolic example. One of the industry’s most customer-friendly brands moved away from long-standing sacred cows like free bags and open seating, turning ancillary monetization into one of the most discussed strategic changes in the airline’s recent history.

The growing relevance of the topic mirrors its commercial impact. Global ancillary revenue reached $157 billion in 2025, equivalent to 15.7% of total airline revenue, up from 9.1% in 2016. So, ancillary revenue is no longer a footnote in the airline business model. It is becoming one of the primary battlegrounds where airlines, including full-service carriers, compete for margin growth and commercial differentiation.

A second driver was the growing importance of distribution. This topic forced its way into the earnings conversation in late 2023 and 2024 as low-cost carriers increasingly clashed with OTAs over customer ownership and control of distribution. Ryanair’s fight against OTA scraping is the clearest example. In our dataset, the keyword “OTA” went from zero mentions in both Q1 2022 and Q1 2023 to 36 mentions in Q1 2024 alone.

2. Fuel: from line item to boardroom obsession

Fuel is the second-fastest growing topic in our analysis, but unlike Ancillary & Distribution, its rise is not driven by a structural change in airline strategy. It’s driven by the simple fact that fuel remains one of the industry’s largest and most volatile cost items.

The topic opened the period loudly back in 2022.

- Russia’s invasion of Ukraine sent oil prices surging in early 2022, pushing fuel-related discussions to nearly 10% of all tracked mentions.

- Much of the conversation focused on hedging positions, fuel price exposure, and how airlines planned to protect margins against rising energy costs.

Then fuel largely disappeared from the spotlight. Between 2023 and 2025, it accounted for just 2-4% of earnings call discussions. Fuel was still there, of course, but mostly as a line item in guidance rather than a strategic talking point. Outside of occasional discussions about hedging programs, particularly among European carriers, executives spent their attention elsewhere.

That changed dramatically in Q1 2026. The Strait of Hormuz crisis and the resulting spike in jet fuel prices pushed fuel to 16.9% of all tracked mentions, making it the single largest topic-quarter in our entire dataset.

Interestingly, the language changed alongside the price environment.

- In 2022, executives primarily talked about hedging programs and fuel-price protection.

- By 2026, the discussion had shifted toward fuel surcharges, capacity adjustments, and the broader commercial consequences of sustained cost pressure.

The sensitivity is hardly surprising. Jet fuel typically accounts for roughly a quarter to a third of airline operating costs. When fuel prices move, airline economics move with them. And when airline economics move, fuel quickly returns to the center of the earnings conversation.

3. Geopolitics & Macro: a new worry every year

Unlike Fuel, where the conversation largely rises and falls with the price of energy, Geopolitics & Macro tells a different story. Here, the worries keep changing:

- In 2022, the conversation was dominated by the aftermath of Russia’s invasion of Ukraine and the resulting inflation shock. Inflation alone was mentioned 40 times in Q1 2022 as airlines grappled with rising costs and growing economic uncertainty.

- During 2023 and much of 2024, the topic faded into broader macroeconomic discussions. Executives focused on interest rates, foreign exchange movements, recession concerns, and the potential impact on consumer demand.

- In 2025, tariffs emerged as a major concern, pushing mentions from near zero to 60 in Q1 alone. “Uncertainty” became one of the defining words of the quarter, helping drive Geopolitics to 18.7% of all tracked mentions (its highest level in the entire analysis period).

- By Q1 2026, the focus had shifted once more, as we all know. Trade concerns gave way to geopolitical conflict, with references to the Middle East and Iran surging to more than 80 mentions, up from only single digits in most previous quarters.

So, while the specific concerns keep changing, geopolitical disruption itself is becoming a more permanent feature of the airline operating environment. As a result, the ability to anticipate geopolitical developments, assess their commercial implications, and react quickly is increasingly becoming part of the strategic toolkit of leading airlines.

In many ways, geopolitical foresight is evolving from a niche planning exercise into a core management capability.

4. From loyalty economics to premiumization

Like Ancillary & Distribution, Premium & Loyalty is a growth story largely driven by management choice rather than external shocks. The difference is that the conversation is less about monetizing the passenger and more about attracting, retaining, and upselling the most valuable ones.

To be clear, parts of this topic are not new.

- Loyalty programs have been among the airline industry’s most important profit drivers for decades, particularly in the United States, where loyalty economics often contribute a significant share of airline profitability.

- Yet the recent rise in earnings-call attention goes beyond traditional loyalty discussions.

The real growth driver is premiumization.

The topic’s share of earnings-call discussion climbed steadily from 8.0% in Q1 2022 to a peak of 19.3% in Q3 2025, driven by airlines’ increasing focus on capturing a larger share of traveler spending through premium products (think business-class and premium-economy seats).

Interestingly, the story started as a demand surprise.

- In the early post-pandemic years, executives repeatedly highlighted the strength of premium leisure demand.

- One carrier reported “record paid load factors in every one of our premium cabins,” driven by demand from customer segments that had historically been far less willing to pay for premium seats.

Over time, the conversation evolved from demand observations to strategic investments.

- Cabin retrofits, premium seating, segmented fare products, lounges, and other upgrades increasingly dominated the discussion.

- The economics explain why. According to McKinsey, premium products typically account for 20% to 30% of full-service airline revenue these days. At Delta Air Lines, premium revenue even overtook main-cabin revenue for the first time in Q4 2025.

The result is a notable shift in how airlines think about value creation. Loyalty remains important, but it is increasingly becoming part of a broader premiumization strategy.

Not every important topic is a growth topic

Of course, we could tell similar stories for many of the themes that did not make it into the four growth categories. Some of them remain fundamental to airline economics despite relatively stable volumes of mentions.

Take Network Planning. It remains the single most-discussed topic in airline earnings calls and arguably one of the industry’s most important capabilities. In today’s environment, airlines constantly adjust networks to cope with rising fuel costs, shifting demand patterns, geopolitical disruptions, and no-fly zones. Finnair’s ongoing network redesign following the closure of Russian airspace is perhaps the most visible European example.

But arguably more interesting than the stable themes are the categories that clearly lost momentum.

In most cases, the explanation is fairly straightforward.

- Fleet discussions cooled after peaking in late 2022, when aircraft delivery delays (especially on Boeing’s side), engine issues, and groundings dominated large parts of the earnings conversation.

- Sustainability followed a similar path. During the early 2020s, climate and emissions topics were firmly at the center of public debate, driven by movements such as Fridays for Future, growing regulatory pressure, and ambitious net-zero commitments across industries. Today, that momentum has clearly cooled. The same shift is visible in airline earnings calls, where sustainability now accounts for less than 1% of tracked mentions. Coincidentally, that is roughly in line with the share of SAF in global jet fuel consumption today.

- Labor followed a similar trajectory, falling from nearly 10% of all tracked mentions in early 2022 to just 1% in the latest quarter as airlines gradually worked through the worst of the post-pandemic hiring crisis.

But there is one declining category that deserves a closer look.

Unlike Fleet, Sustainability, or Labor, its loss of momentum feels distinctly counterintuitive.

That category is AI & Digital.

Why AI barely shows up in airline earnings calls

Given the current AI hype cycle, this is arguably the most surprising finding in our analysis.

Artificial intelligence is undoubtedly emerging as one of the defining technologies of our era. Millions of travelers already use AI tools to research and plan trips (even if adoption estimates still vary significantly across studies). Technology leaders describe AI as a generational platform shift. And hardly a week goes by without a new announcement about AI transforming travel search, booking, customer service, or airline operations.

Yet none of that is clearly visible in airline earnings calls.

- Across the entire four-year period, AI & Digital was the least-discussed topic cluster in our analysis, accounting for just 1.6% of all tracked mentions.

- Its share of earnings-call discussion actually declined from 1.3% in Q1 2022 to just 0.6% in Q1 2026, the quietest quarter for the topic in two years.

At first glance, that seems counterintuitive. But there is a simple explanation: earnings calls are ultimately conversations about commercial performance. While AI may already be influencing how travelers search for trips and how airlines experiment with new operational tools, its impact on the bottom line remains limited for now.

At the same time, we should be careful not to overinterpret the findings. This is also where our methodology reaches its limits.

The challenge is that AI rarely appears as a standalone strategic theme. Instead, it increasingly shows up inside other conversations.

- In distribution discussions, for example, one legacy carrier was asked directly how it planned to sell through large language models and whether future AI-powered travel agents would connect through APIs, GDSs, or other existing infrastructure.

- A low-cost airline CEO went even further, suggesting that ChatGPT-like technologies could one day become a dominant marketplace layer between airlines and travelers.

The same pattern appears in other categories.

- In revenue management discussions, airlines increasingly reference generative AI and machine learning as tools for dynamic pricing and commercial optimization.

- In operational discussions, AI is frequently framed as a way to improve customer experience, automate workflows, and increase workforce efficiency.

The key point we’re making: AI may not yet be large enough to dominate the earnings conversation on its own. But it is already leaving footprints across several of the industry’s most important strategic themes. That makes it less visible in a topic-based analysis, but not necessarily less important.

Whether those footprints evolve into a dedicated earnings-call topic of their own remains to be seen.

What is clear, however, is that AI is beginning to weave itself into the fabric of airline strategy.

And that is exactly why we will be tracking it more closely in future editions of this analysis.