Long-time TNMT readers might remember that unicorn mappings used to be one of our favorite research perspectives.

Why?

Because few lenses reveal emerging shifts in Travel and Mobility Tech as clearly as looking at which technology startups cross the billion-dollar valuation mark.

Unicorns are rarely random.

They tend to emerge where investor conviction, technological momentum (or hype), and changing customer behavior suddenly align.

And this is worth tracking, because in many cases, the startup ecosystem surfaces structural market transitions years before public markets fully recognize them.

That’s why it’s high time for a new unicorn update.

Our last major mapping is now almost two years old.

And importantly, the market environment has changed dramatically since then.

- Back in the post-COVID funding boom, unicorn status had started to lose meaning.

- Cheap capital flooded the venture ecosystem, valuations exploded, and startups reached billion-dollar paper valuations with very limited commercial traction and highly theoretical business outlooks.

- At one point, it felt like every second pitch deck claimed to be “the next unicorn.”

The exclusivity of the club disappeared.

And with it, much of the analytical value.

But today, the picture looks very different:

- Capital is scarcer again.

- Growth expectations are harsher.

- IPO markets remain difficult.

- And downrounds, shutdowns, and consolidation have fundamentally reshaped the startup landscape.

In other words: becoming a unicorn in 2026 actually means something again.

This makes the current unicorn landscape significantly more interesting than it was during the funding excesses of 2021 and 2022.

And perhaps even more importantly: The new generation of Travel and Mobility Tech unicorns tells us something profound about where innovation in our industry is actually heading.

So without further ado, let’s look at the unicorn changes over the past few years.

From unicorn boom to unicorn filtering

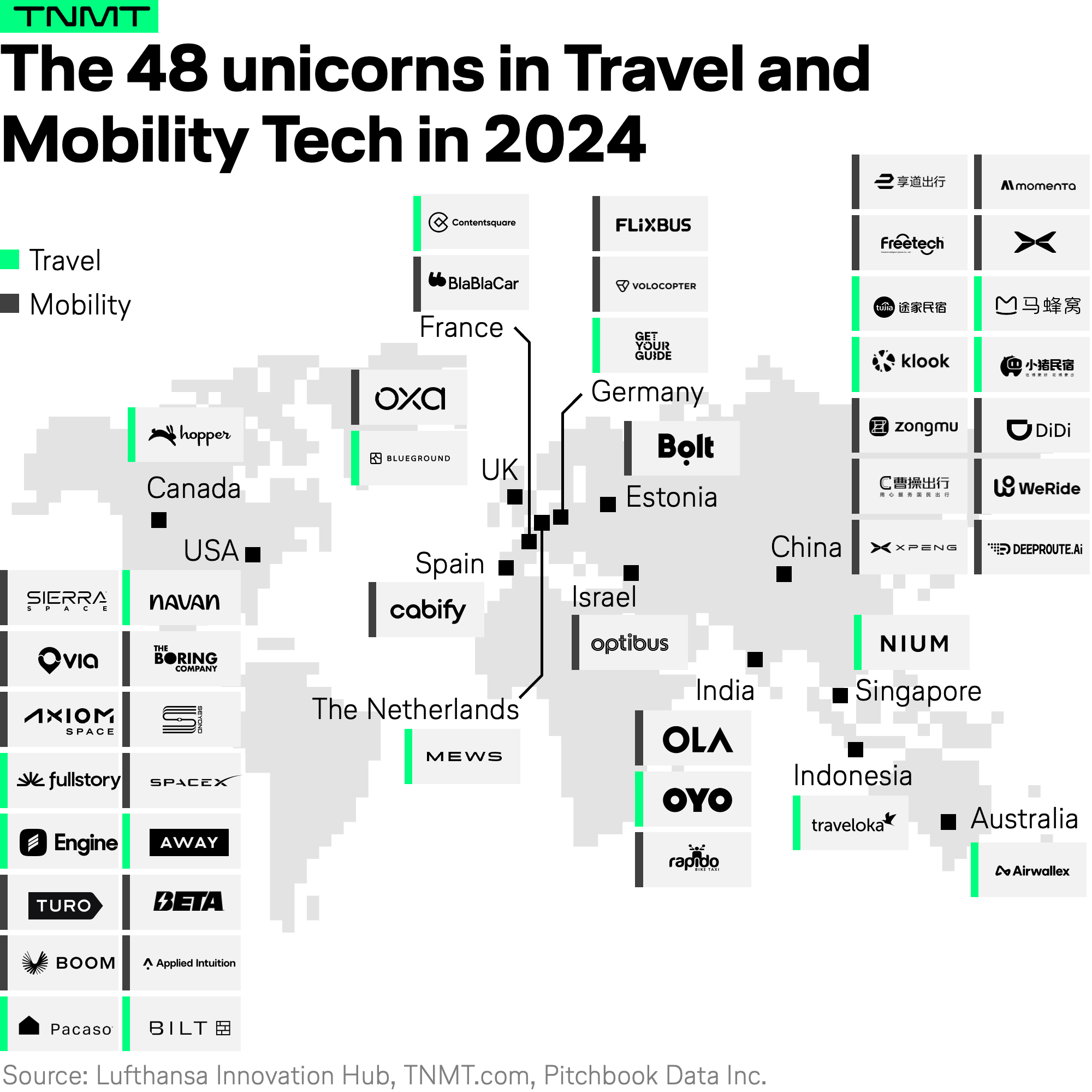

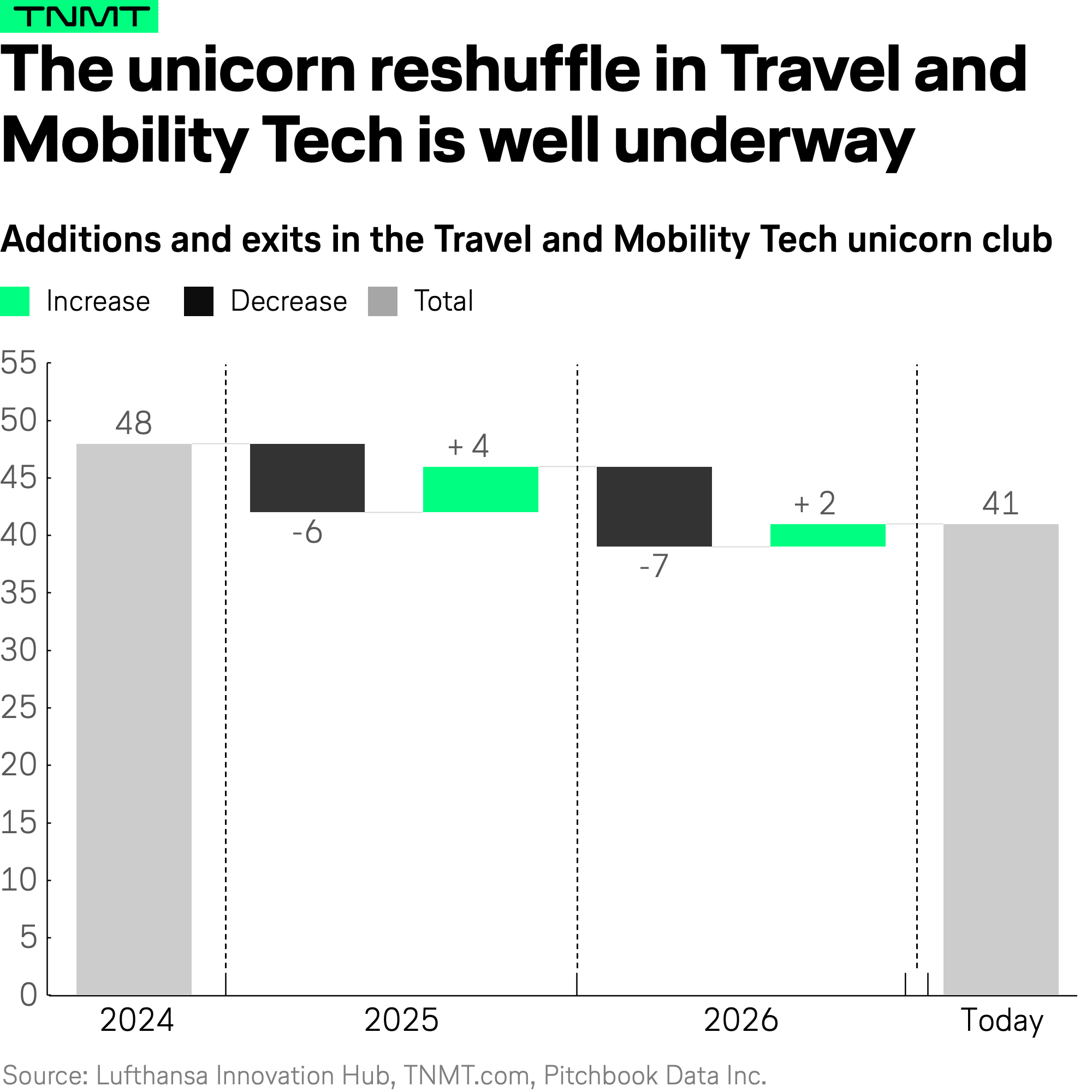

For context up front, and to get things straight, here’s how the Travel and Mobility Tech unicorn club looked just two years ago.

Back in 2024, we counted 48 privately held startups in our sector valued at more than $1 billion USD.

At the time, two major patterns stood out:

- First, the unicorn landscape was still heavily dominated by Ground Mobility, especially autonomous driving and related on-demand mobility players.

- Second, the broader unicorn club was already stagnating after the post-COVID funding excesses of 2021 and 2022.

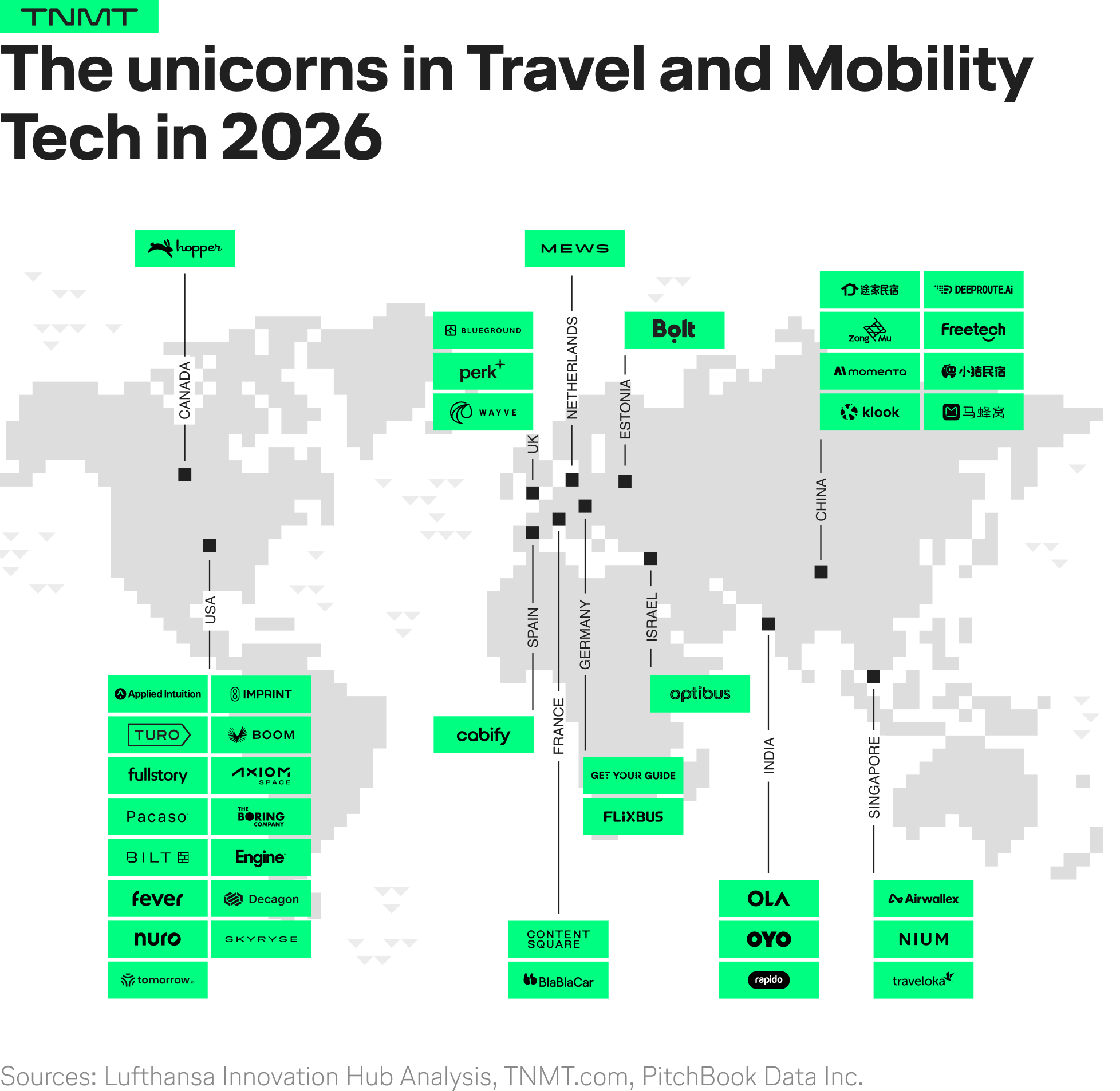

Fast forward to today, and the club has shrunk further.

As of May 2026, we count 41 Travel and Mobility Tech unicorns globally.

But the underlying movement is much more dramatic than the net decline of seven companies suggests.

Beneath the surface, the unicorn club has undergone a meaningful reshuffling, with 13 firms exiting while a completely new set of 6 startups has entered the ranks.

In all fairness, not every exit reflects failure or valuation collapse.

- Some firms effectively aged out of the startup category despite remaining privately held. The most prominent example is SpaceX, founded back in 2002 and now operating more like a mature industrial giant than a traditional startup.

- Others gradually drifted away from core Travel and Mobility use cases into broader adjacent markets; for example, Away, which shifted beyond its original “smart luggage” positioning into a non-tech-focused lifestyle and consumer brand.

Notably, roughly half of all unicorn exits occurred through public market transitions (IPOs), with most of those companies in the Ground Transportation sector.

One important travel-focused exception was Navan, whose trajectory reinforced how enterprise travel evolved from a simple booking category into a much broader infrastructure layer around payments, expense management, and workforce mobility.

What all of this ultimately shows is that the unicorn club isn’t just getting smaller; it’s being replaced.

And the newcomers entering the club today look very different from the unicorns that dominated the previous cycle.

That’s where things start to get really interesting.

The real story sits beneath the category breakdown

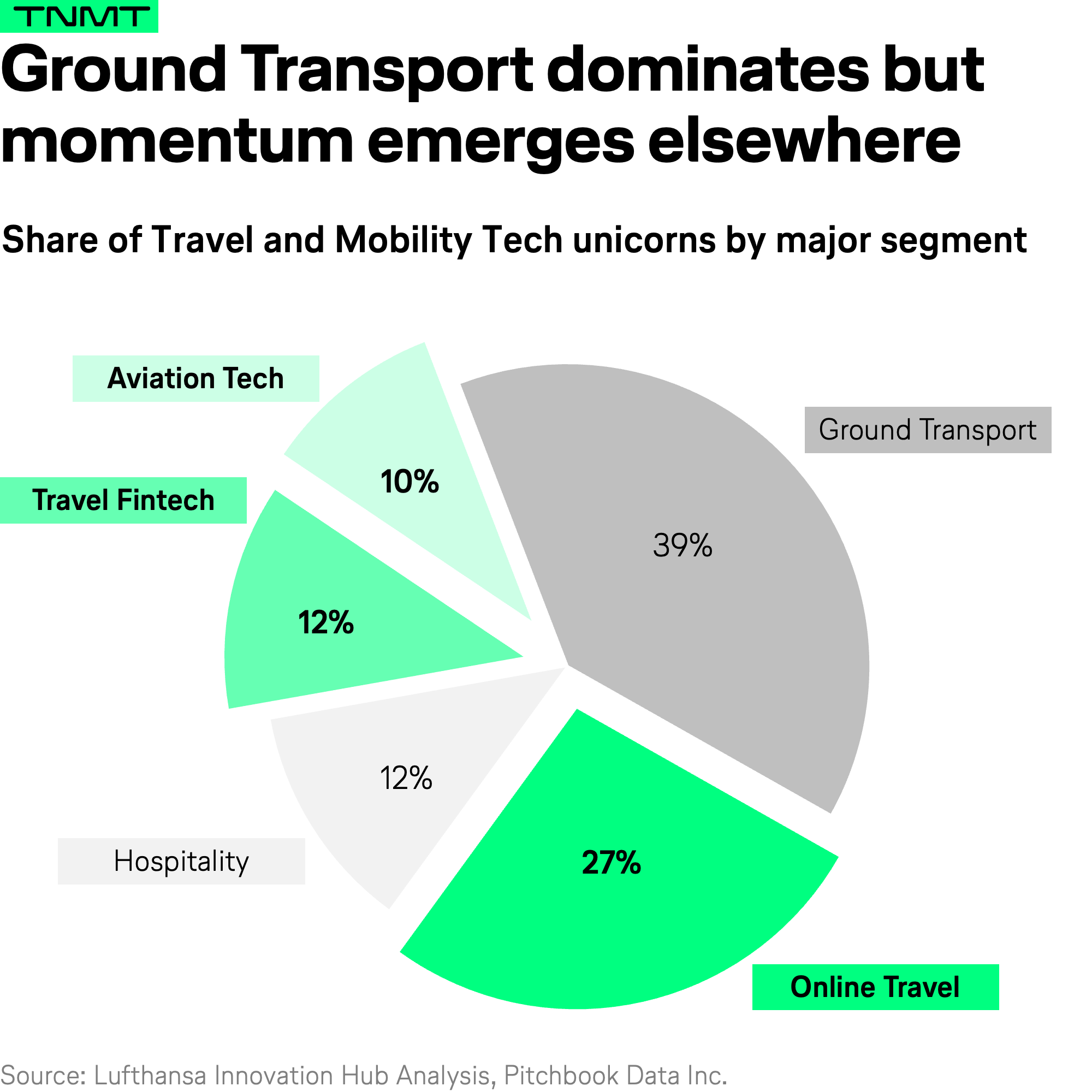

At first glance, this reshuffling may not immediately stand out when looking at the high-level category distribution of today’s 41 unicorns.

As shown below, the majority of unicorns in Travel and Mobility Tech still belong to the broad Ground Transportation category.

That includes:

- Ride-hailing players.

- Autonomous driving providers.

- And ground mobility challengers like FlixBus and others.

None of this is particularly surprising.

Ground transportation has dominated startup funding for more than a decade, largely because mobility problems are frequent, urban, and enormous in scale.

Autonomous driving alone continues to absorb vast amounts of capital and investor attention.

But that’s not the most interesting signal hiding in today’s unicorn club.

The more important development is happening elsewhere.

For the first time in years, we’re seeing meaningful new unicorn formation in segments much closer to the core of the traditional travel and airline business itself.

These segments include:

- Aviation Tech.

- Online Travel.

- And Travel meets Fintech.

Let’s zoom in on each of those segments.

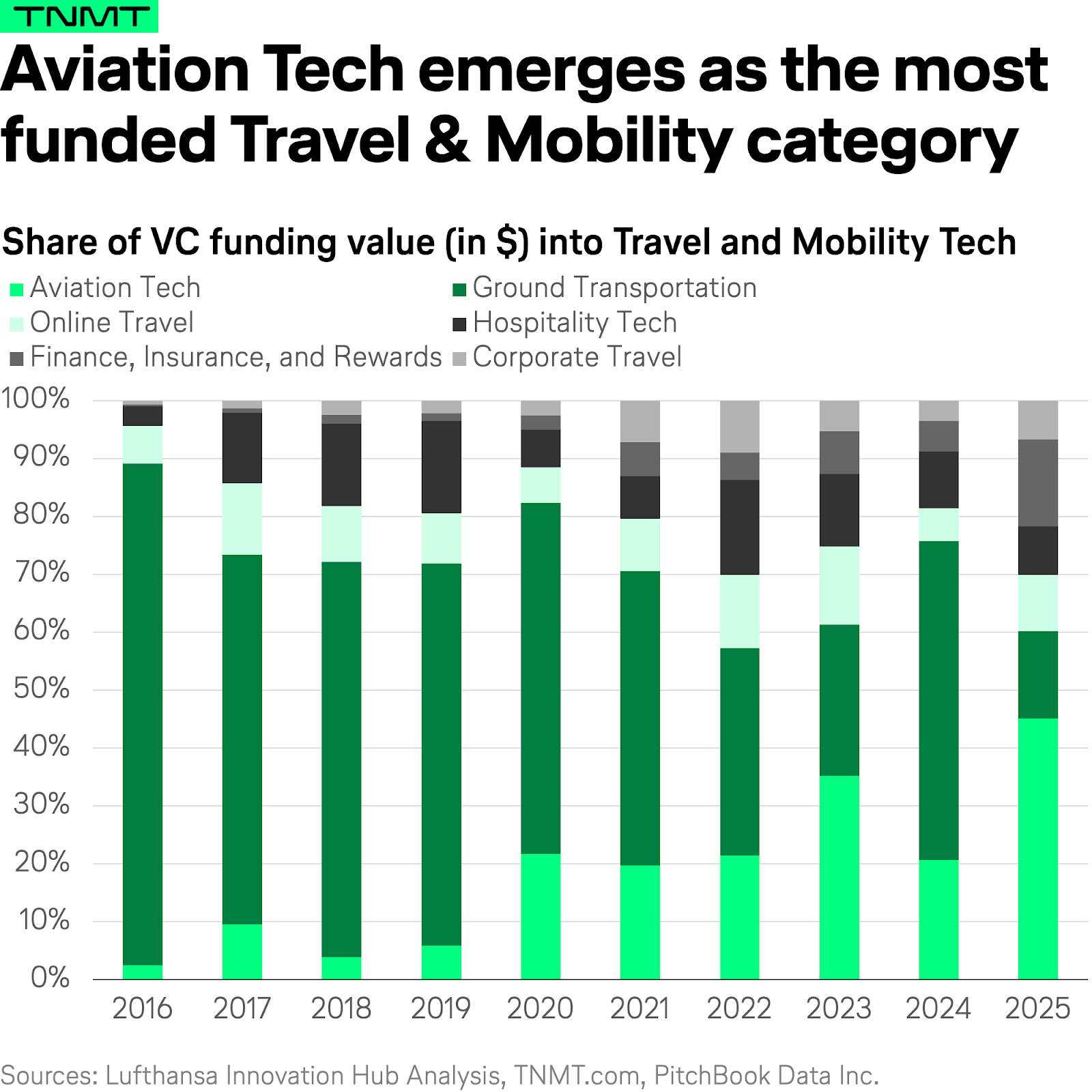

Aviation Tech: The biggest opportunity pocket in Travel and Mobility Tech

If you remember our recent full-year analysis of venture capital investment trends across Travel and Mobility Tech, you might also remember one of our clearest conclusions:

Aviation Tech has become the industry’s biggest opportunity pocket.

And the funding data backs that up:

- In 2025, aviation-focused startups captured almost half of all venture capital dollar volume across Travel and Mobility Tech.

- That made Aviation Tech the single most funded category in our ecosystem.

For regular TNMT readers, it therefore probably won’t come as a major surprise that Aviation Tech also produced several of the most notable new unicorns over the past two years.

What is surprising, however, is the type of Aviation Tech companies joining the club this time around.

Because, unlike the previous cycle, which was dominated by flashy eVTOL visions, hypersonic aircraft concepts, and urban air mobility hype, the newest Aviation Tech unicorns sit much closer to the operational heart of aviation itself.

Take Tomorrow.io. At first glance, a weather forecasting company may not sound like the most exciting unicorn candidate in aviation. But in reality, weather remains one of the single largest sources of operational disruption for airlines globally.

Traditional forecasting systems were never designed to answer the kinds of hyper-granular operational questions airlines increasingly need answered in real time:

- Which specific aircraft turnaround is at risk?

- Which passengers should proactively be rebooked?

- Which gate operations will be impacted by convective weather in the next 45 minutes?

That’s the resolution gap Tomorrow.io is trying to solve.

The company originally started as a data intelligence platform, aggregating unconventional weather signals (from connected cars and IoT devices to cell towers) to create hyperlocal forecasting models powered by AI.

But the more interesting evolution came later.

- Tomorrow.io is now building its own low-Earth orbit satellite constellation called DeepSky, designed to provide high-frequency atmospheric data updates globally.

- By early 2026, the company had already launched 13 satellites into orbit.

In February 2026, Tomorrow.io raised $175 million in a funding round, officially earning unicorn status. And importantly, major airline customers already include our parent company, Lufthansa, and JetBlue.

The message we want you to take away from this:

The next wave of Aviation Tech is about building the intelligence and infrastructure layers that make aviation operations smarter, faster, and more resilient.

And be assured, Tomorrow.io isn’t the only example.

Another standout newcomer is Skyryse.

The company essentially aims to become an operating system layer for aviation.

- Its technology replaces dozens of traditional cockpit controls (think of gauges, switches, and levers) with software-driven flight systems powered by multiple onboard computers.

- The goal isn’t fully autonomous flight (at least not yet) but rather simplifying the most dangerous and complex aspects of aircraft operation.

Think less “pilot replacement” and more “pilot augmentation.”

For now, Skyryse focuses primarily on smaller aircraft and rotorcraft applications rather than large-scale commercial aviation.

But the underlying direction is clear: Software is increasingly becoming the defining layer of aviation innovation itself. And that may ultimately prove much more transformative than simply building faster aircraft.

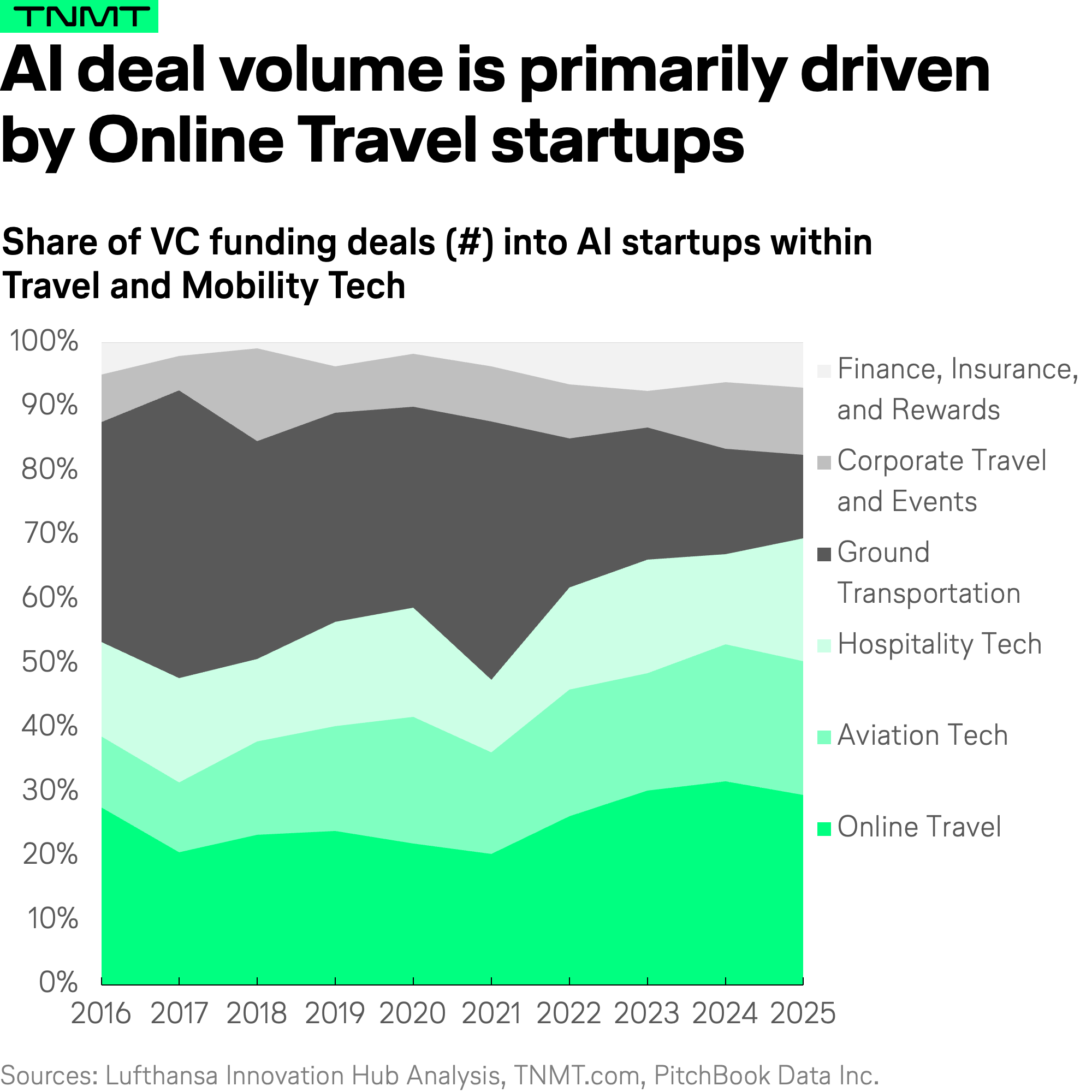

Online Travel: AI’s most active battleground

Speaking of software and AI, but this time on the customer-facing side of travel, we also saw an important new unicorn emerge in the Online Travel segment.

And importantly, the broader funding data already hinted that this was coming.

As part of our 2025 venture capital analysis, we identified Online Travel as the single most active AI investment segment in Travel and Mobility Tech by deal count.

- In 2025, roughly 30% of all AI-related startup deals in Travel and Mobility Tech went into Online Travel companies

- This makes Online Travel the largest AI segment in the industry, even ahead of Ground Transportation.

What does that mean?

It means more AI-focused startups are currently being funded around the inspiration, planning, booking, and servicing layers of travel than in any other sub-sector.

This isn’t particularly surprising.

- Customer service and itinerary management remain among the most obvious (and commercially valuable) applications for Gen AI in travel.

- The industry still operates with enormous operational complexity, fragmented systems, and millions of repetitive customer interactions every day.

Which brings us to Online Travel’s latest unicorn: Decagon.

Founded only in August 2023, the company reached unicorn status in less than two years after raising a $250 million late-stage funding round in January 2026 at a valuation of $4.5 billion USD.

That alone is remarkable.

But what makes Decagon strategically interesting is what kind of AI company it represents.

- Decagon positions itself as an AI concierge platform, helping enterprises deploy conversational voice and chat agents for customer requests.

- In travel, its systems support itinerary management, booking assistance, and loyalty interactions.

- Current customers already include Hertz, Avis, and travel rewards company Bilt.

And unlike many incumbents now layering AI onto legacy software stacks, Decagon is fundamentally GenAI-native, meaning the company was born in the large language model era.

There is no pre-AI legacy product underneath. The entire platform is built around conversational AI agents as the core operating layer.

That distinction matters.

Since our original funding analysis, Decagon has also introduced what may be its most important feature yet: persistent customer memory.

- Conversations no longer restart from zero every time a traveler reaches out.

- Instead, customer context carries across interactions, creating something much closer to a longitudinal relationship layer rather than a transactional support tool.

And that may ultimately be the bigger shift hiding underneath the AI hype.

The next generation of Online Travel platforms may no longer primarily compete on inventory. They may compete on memory. And the companies building those relationship layers early are increasingly becoming some of the most valuable startups in the entire Travel and Mobility ecosystem.

Travel Fintech: the next loyalty battleground

And last but not least, let’s talk about the intersection where fintech meets travel.

Think:

- Payments.

- Insurance.

- Rewards.

- And especially loyalty infrastructure designed around travel behavior.

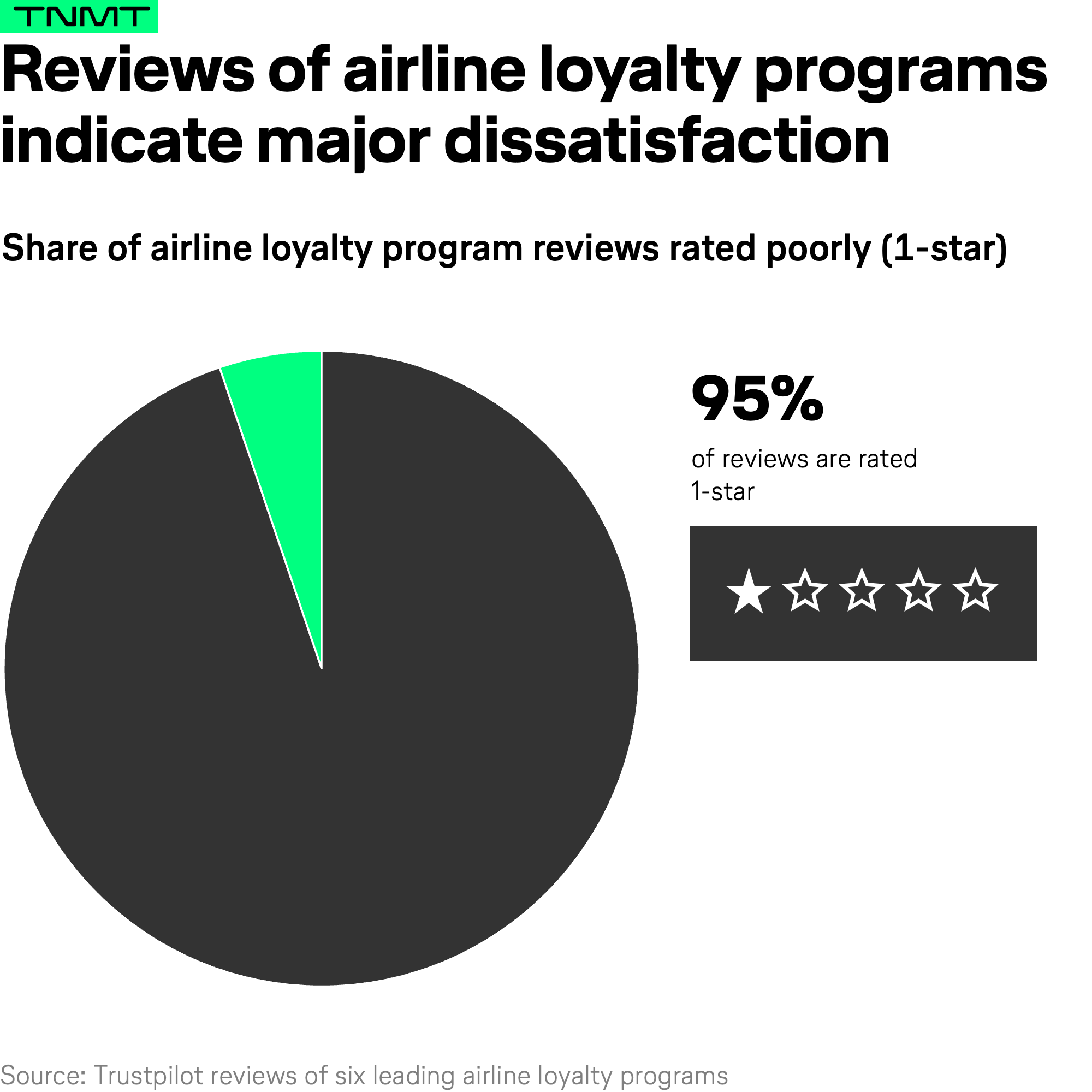

This segment is becoming increasingly important as well, particularly for airlines.

Because while airlines generate billions of dollars through loyalty programs and co-branded credit cards, customer satisfaction with those programs remains surprisingly poor, as we highlighted in a previous TNMT analysis.

That disconnect is creating opportunity.

A new generation of startups is trying to rethink what travel loyalty actually looks like in a world shaped by digital payments, embedded finance, and AI-driven personalization.

One of the most notable new unicorns in this category is Imprint.

- At first glance, Imprint looks like a fintech infrastructure company. And technically, that’s exactly what it is.

- The firm operates a B2B2C model that helps consumer brands launch and manage co-branded credit card programs across retail, hospitality, and travel.

But the strategic relevance goes much deeper.

For decades, the co-branded airline card market has largely been controlled by a handful of incumbents like Chase, American Express, and Barclays, all operating through entrenched, multi-decade relationships with giants like United, Southwest, American, and IHG.

Imprint is trying to break that model open.

Its proposition is surprisingly simple:

- Faster card rollout.

- Better loyalty integration.

- And significantly stronger data ownership for the brand itself.

That matters because it potentially democratizes access to one of the most profitable ecosystems in travel.

Until now, many mid-sized travel brands simply weren’t large enough to secure major co-branded card partnerships with the traditional banking giants.

Imprint changes that.

And the economics behind this market are enormous.

The global co-branded airline card segment was worth roughly $14.6 billion in 2024, according to Research and Markets.

Turkish Airlines became Imprint’s first major airline partner in 2024, and the early results sound impressive:

- 78% of cardholders became active users.

- 83% of spending happened outside the airline ecosystem itself.

That second metric is especially important.

Because the true financial power of airline credit cards has never been ticket purchases. It’s everyday spending across groceries, restaurants, and retail.

In other words: airlines increasingly must make money when customers aren’t flying.

And that may ultimately explain why Travel Fintech is quietly becoming one of the most strategically important sub-segments in the entire Travel and Mobility stack.

The age of boring winners

So what does the current unicorn landscape actually tell us about where Travel and Mobility Tech is heading?

The previous unicorn cycle was dominated by highly visible consumer narratives around ride-hailing, micromobility, autonomous driving hype, and futuristic transportation concepts.

Today’s newcomers look very different.

Increasingly, they operate deeper within the industry stack itself (think operational intelligence and AI-servicing layers). We could also say: the next generation of Travel and Mobility Tech winners is increasingly focused on making the industry run better (not just look more exciting from the outside).

And perhaps that’s exactly why unicorn tracking suddenly feels relevant again.

The newest billion-dollar startups increasingly look like early indicators of where the strategic priorities of the entire industry are heading next. Right now, those signals point toward a much more operational, software-driven, and infrastructure-centric future for travel.